The public discourse surrounding executive compensation centres on a provocative question: Are CEOs worth what they are paid? Critics point to the widening gap between executive pay and average worker wages as evidence of rent-seeking behaviour or ‘pay for luck’, where executives reap rewards from favourable market tailwinds they did nothing to create (Frydman and Saks 2010, Schenen and Amore 2020). Proponents of current compensation structures argue that the value of good leaders is proportional to the size of firms they lead, and as firms grow larger, elite managerial talent becomes even more valuable.

It is suggestive that the period in which CEO pay rose rapidly also corresponds to one in which firms and labour markets have been profoundly reshaped by global forces.

Can global shocks change the contract between a firm and its leader, and can we use these shocks to answer the fundamental question of whether CEOs are worth what they are paid?

Our recent research (Hummels et al. 2026) addresses these questions by merging two traditionally distinct modelling frameworks: the principal-agent model (which focuses on unobservable effort and risk) and the assignment model (which focuses on matching high-ability individuals with large firms). Using two decades of Danish worker-firm data combined with data on executives and their compensation, we provide evidence that globalisation doesn't just increase pay – it fundamentally changes why and how CEOs are compensated.

The scale effect: Globalisation as a force multiplier

The ‘assignment’ literature (Gabaix and Landier 2008, Tervio 2008) predicts that CEO pay should scale with firm size because the marginal impact of a CEO's talent is magnified by the resources they control. Global markets enable the best firms to grow larger, widening the size distribution of firms and the pay of their leaders.

A challenge with this literature is that the assignment effect is typically identified using cross-sectional correlations between pay and size and lacks independent information on the ability of leaders. Sorting out the contribution of global markets to firm size and CEO pay is particularly problematic if a firm’s productivity changes over time for reasons unrelated to CEO talent or effort. More productive firms engage in more trade, get larger, and pay all workers (including managers) more.

To resolve this identification challenge, our study utilises shocks to the world trade environment that are exogenous to individual firms but, because of the specialised way firms offshore and import, have differential impact on firms. We find that:

- Changes in the global environment lead to exogenous increases in exporting and offshoring and that leads to significant increases in firm sales and value. Export sales in our data were responsible for more than half of their overall firm growth.

- This growth translates directly into CEO pay. Within the same CEO job spell, the pay-to-firm-value elasticity is 0.28 (0.63 for firms with at least 100 employees). Bonus payments to CEOs are 2-3 times more firm-value-elastic.

The volatility effect: Incentivising effort in a noisy world

Standard principal-agent models of this problem (see Chaigneau et al. 2023 for discussion and extension) ask how firms should compensate leaders when CEO effort affects firm value but effort is difficult to observe and separate from changes in the competitive environment. The standard solution is to pay the CEO a share of firm value that is decreasing in the volatility facing the firm.

We find the opposite: volatility induced by global shocks increases the share of firm value paid to the CEO. We also find that the share of firm value paid to the CEO is rising in the size of the firm, effectively doubling the impact of scale on pay.

The reason lies in the nature of the shocks. We distinguish between ‘additive’ shocks (changes in firm value that occur regardless of what the CEO does) and ‘interactive’ shocks (opportunities that require additional CEO effort to capture). The optimal contract in this environment actually puts more weight on changing firm value when volatility is high and firm size is large, provided that volatility comes from shocks that interact with executive effort.

The ability effect: Is it ‘pay for performance’?

Perhaps the most important question for boards and policymakers is whether high-paid CEOs actually deliver better results. To answer this, we measure ability in two ways and ask three questions. Do higher-ability CEOs sort into larger firms, are they paid more, and do they generate greater value when the firm is hit by exogenous global shocks?

Our two measures of ability are (1) an ‘AKM fixed effect’ from Abowd et al. (1999) (how well the person was paid in their jobs before they became CEO), and (2) their actual years of CEO experience. The results differed significantly depending on which ability measure we used.

Prior pay (AKM): Firms pay a premium for CEOs who were high earners earlier in their careers, and these individuals tend to sort into larger firms. However, we found little evidence that these historically well-paid individuals actually generate better outcomes or respond more effectively to shocks. This suggests that some portion of CEO pay may indeed be driven by a prestige or credentialing effect rather than pure productivity.

Experience: More experienced CEOs do not sort into larger firms, but they are paid more for each year of experience, generate higher sales and firm value in all periods, and generate particularly large increases in value when the firm is hit with global shocks.

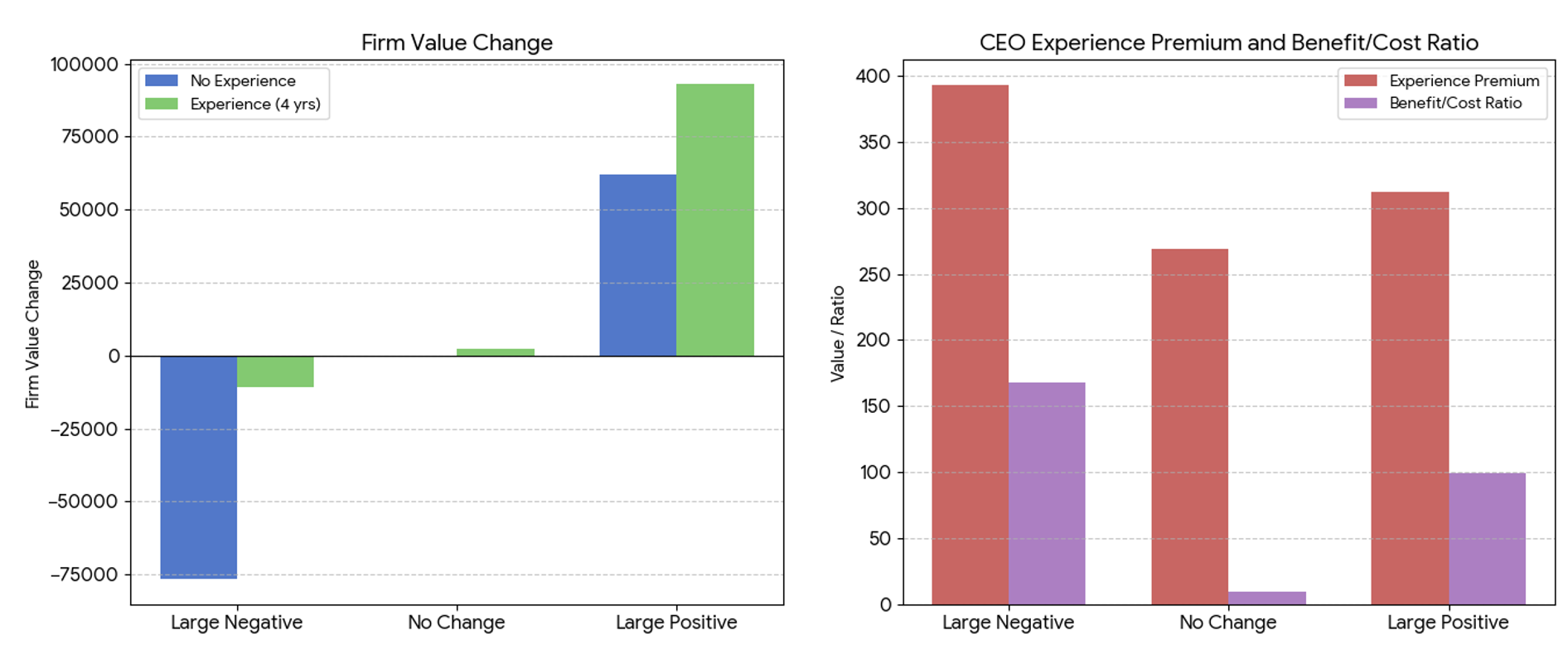

Experienced CEOs act as both a magnifier and a shield. When a firm is hit with a large positive demand shock, an experienced CEO translates that tailwind into much larger sales and value gains than an inexperienced one. In the face of a large negative shock experienced CEOs significantly mitigate the losses. A large negative shock that might reduce firm's value by 15% can be entirely counteracted by a CEO with just five more years of experience.

The ability to magnify positive or shield negative shocks to firm value holds even when we look at the same individual CEO in the same firm, comparing their performance early versus late in their job tenure.

Figure 1 shows the change in firm value (in 1000s of Danish krone) associated with demand shocks of various sizes, comparing a CEO with no experience to one with four years of experience. It then calculates the additional amount (1000s of Danish krone) that is paid to the experienced CEO relative to their inexperienced counterpart, incorporating both the experience premium and the change in firm value that is shared with these leaders. It also calculates a benefit to cost ratio of employing the more experienced CEO.

Figure 1 Change in firm value associated with demand shocks, by experience of CEO (1000s of Danish krone)

Perhaps the most striking finding of our research is the sheer magnitude of the value created by experienced leadership. While experienced CEOs are better compensated, the increase in firm value they offer is over 100 times greater than the additional pay they receive. But this accrues primarily when the firm faces large changes in global demand for its products.

Our findings suggest that the common ‘pay for luck’ critique requires more nuance. While it is true that CEOs receive higher pay when global conditions are favourable (which might look like luck), our data are consistent with the idea that boards write contracts that reward the effort required to capitalise on those favourable conditions.

Moreover, we find a U-shaped response to shocks. This is consistent with the idea that CEOs work hard during good times to maximise their share of the gains, but they also work exceptionally hard during bad times. Why? We show in an extension of our model that higher ability CEOs want to avoid being fired and losing their future CEO premium. This ‘loss mitigation’ is a critical part of what makes an executive valuable to shareholders.

Conclusion and policy implications

For those concerned with the policy implications of executive pay, our research offers a complex picture. We find that the rise in CEO pay can be explained by the expanding scale of firms and the increasing volatility of the global environment.

However, the fact that experience generates a 100:1 return while prior salary (the AKM fixed effect) does not, suggests that there is room for improvement in how boards identify and price CEO ability.

References

Abowd, J M, F Kramarz, and D N Margolis (1999), “High wage workers and high wage firms”, Econometrica 67(2): 251-333.

Chaigneau, P, A Edmans and D Gottlieb (2023), “A theory of fair CEO pay”, VoxEU.org, 27 January.

Frydman, C and R E Saks (2010), “Executive compensation: A new view from a long-term perspective, 1936-2005”, Review of Financial Studies 23(5): 2099-2138.

Gabaix, X and A Landier (2008), “Why has CEO pay increased so much?”, Quarterly Journal of Economics 123(1): 49-100.

Hummels, D, J R Munch, and H Zhang (2026), “Using Global Shocks to Understand the Level and Structure of Executive Compensation”, NBER Working Paper No. 35004.

Hummels, D, R Jørgensen, J Munch, and C Xiang (2014), “The wage effects of offshoring: Evidence from Danish matched worker-firm data”, American Economic Review 104(6): 1597-1629.

Schwenen, S and M D Amore (2020), “The value of luck in the labour market for CEOs”, VoxEU.org, 9 August.

Terviö, M (2008), “The difference that CEOs make: An assignment model approach”, American Economic Review 98(3): 642-668.