The United States is a consumption-driven economy. But over the last half century, the US consumer has been weakening in the face of social and economic pressures.

In recent years, the US Federal Reserve’s easy money policies along with fiscal stimulus have boosted consumption, but with inflation’s resurgence post-pandemic, such measures have run their course and consumer spending has resumed its long-term trend of declining growth. This will likely lead to recession.

What’s the alternative? A US iteration of Japanification in which the Fed, the federal government, or some combination thereof artificially keep the US consumer afloat.

A Consumer-Driven Economy

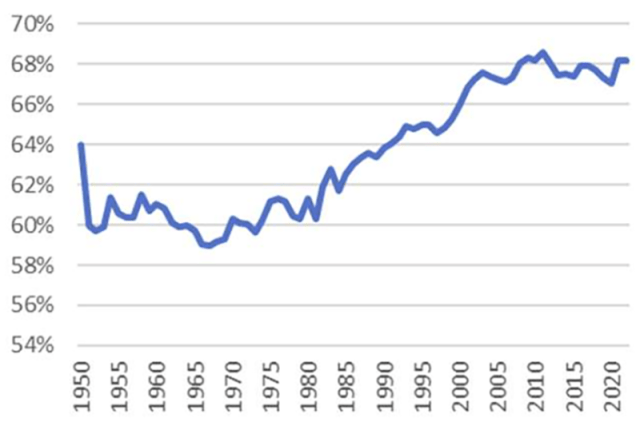

Just how consumer-driven is the US economy? Personal consumption expenditures (PCE) constitute two thirds of total GDP, while gross exports account for only about 10%. The US economy is inward-focused and does not rely much on external income. As such, the consumer’s central role has only become more central over the last 50 years.

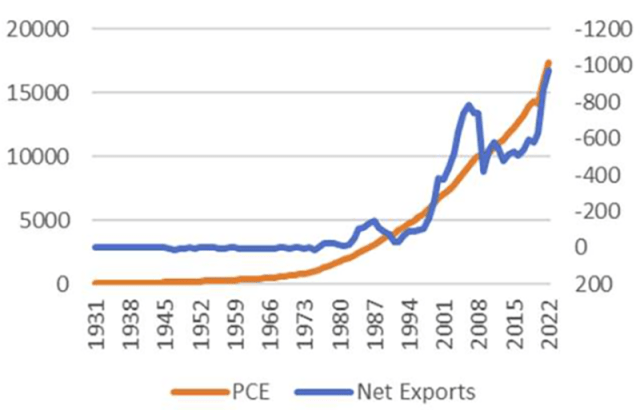

As a share of US GDP, PCE has grown from 59% in 1968 to 68% in 2022, while net exports have fallen and gone into deficit over the same time period, from 0.1% in 1968 to -3.3% in 2022. This export deficit tracks consumption, indicating that it too is now consumer driven.

PCE as a Percentage of US GDP

Sources: Chart data culled from US Census Bureau, BEA, BLS, FRED, BIS

With a Weakening Consumer

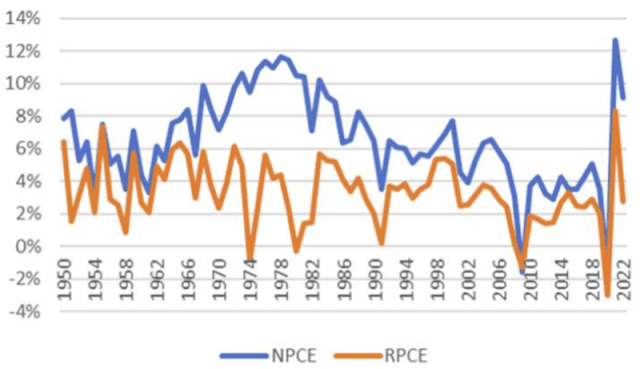

But the US consumer is facing steady and increasing headwinds. While PCE has increased as a share of GDP, both nominal and real PCE growth has slowed over the last half century. Nominal PCE growth declined from 9.9% in 1968 to 3.5% in 2019, and real PCE growth from 5.7% in 1968 to 2.7% in 2022. This indicates that the US consumer’s economic influence is diminishing.

Net PCE (Left Axis) vs. US Net Exports (Right Axis), Both in US Billions

Dovish monetary policy and government stimulus have fueled PCE growth since 2000. These policies went into overdrive amid the COVID-19 pandemic, leading to a sharp jump in nominal PCE growth and a spike in inflation. But those policies cannot be sustained in the face of higher interest rates.

Nominal YoY PCE vs. Real YoY PCE

What Is Ailing the US Consumer?

1. Slower Income Growth

PCE growth has been accompanied by expanding household debt, especially after 1968, and the US consumer is increasingly debt dependent. Household debt now accounts for more of nominal PCE, rising from 73% in 1976 to a peak of 141.5% amid the Great Recession in 2008. As of 2022, it stood at 109%. Debt is growing as a share of PCE, and thus the US consumer is more levered with less capacity to spend.

YoY Household Debt vs. Nominal YoY PCE

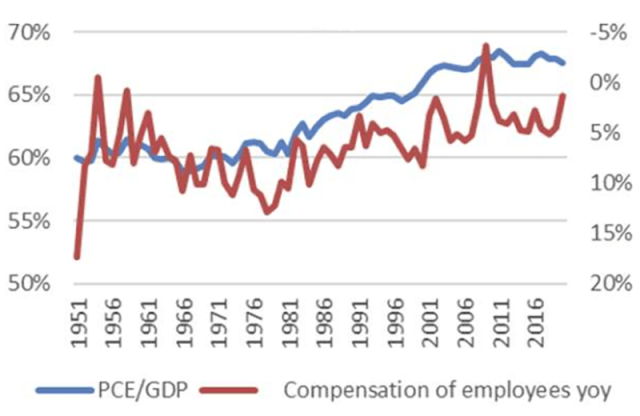

2. Weakness in Other Economic Drivers

PCE has risen as a proportion of GDP even as it has expanded at a slower rate. This implies that the pace of growth of other components of GDP — net exports and capital expenditure (CapEx), for example — has been declining even faster. Moreover, as PCE has taken up an ever greater share of GDP, US wages have not kept pace.

PCE/GDP (Left Axis) vs. YoY Employee Compensation (Right Axis)

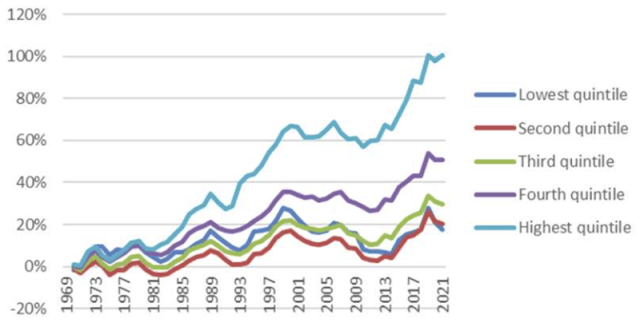

3. Rising Inequality

In a consumption-driven economy, increasing inequality reduces the resources available to a greater and greater proportion of the population and, consequently, reduces overall consumption. According to US Census Bureau estimates, US inequality has risen over the last 50-plus years, with the country’s GINI inequality index increasing from 0.394 in 1970 to 0.488 in 2022. The income of the top 10% of US households has jumped from 213% to 290% of the median household income over the same period. As wealth is concentrated among a smaller and smaller cohort, the purchasing power of the majority diminishes.

Mean Household Income Growth by Quintile

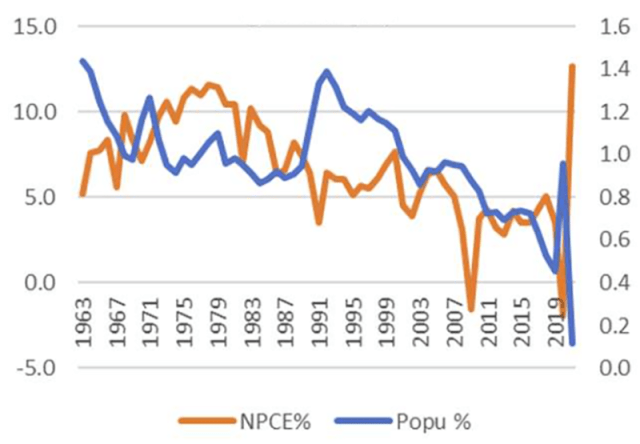

4. Demographic Challenges

The rate of US population growth has been on a fairly consistent downward trend since the 1960s. This means the population is aging and will have a lower share of young people to drive consumption. Both nominal and real PCE growth have tracked lower population growth during the last 50 years.

Nominal YoY PCE Growth (Left Axis) vs. Nominal YoY Population Growth (Right Axis) (%)

So, What Are the Implications?

Taken together, these factors point to four key developments:

1. Slowing Real PCE Growth

Real PCE growth has fallen back to pre-pandemic levels following the COVID-19 bump. To be sure, health care, online services, travel, and auto sales, among other sectors, are defying the trend, but they are the exceptions.

Real YoY PCE Growth Percentage (%)

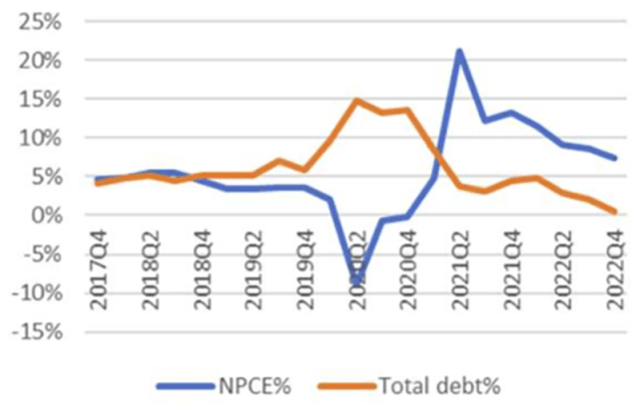

2. A Shifting Debt Burden

Following the global financial crisis (GFC) and again during the pandemic, the federal government increased its debt burden to prop up the struggling consumer and keep the economy running. Thus, the debt burden propelling economic growth shifted from the consumer to the public sector, and PCE growth started tracking total debt more than household debt.

Nominal PCE YoY vs Total Debt YoY

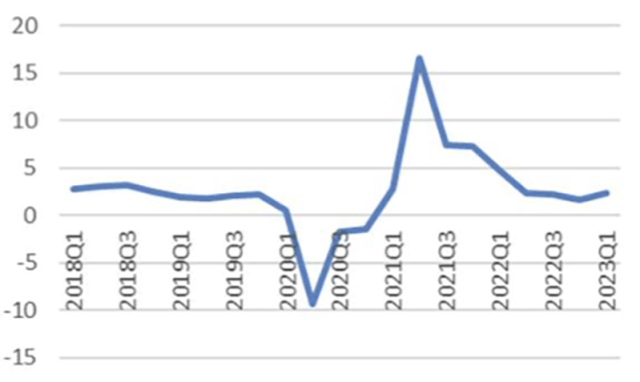

But this phase of increased government spending has come to an end in the face of higher interest rates. Currently, debt growth is falling in all non-financial sectors — government, households, and corporates — as is PCE growth. Meanwhile, delinquency rates on consumer loans have increased, returning to their pre-COVID levels. The COVID-bump in government stimulus has run its course, and the consumer is once again swimming against the current.

Consumer Loan Delinquency Rates (%)

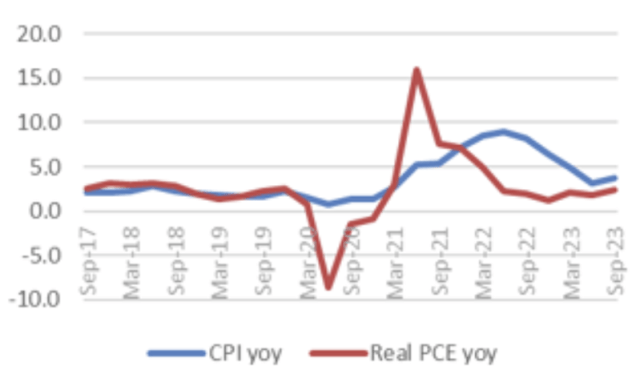

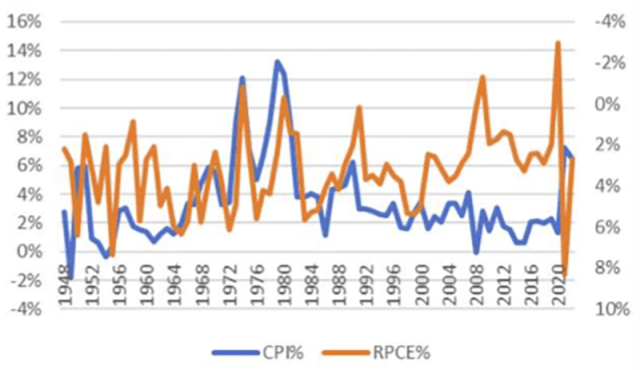

3. Falling Inflation

When consumption growth slows, demand-side inflation does as well. Supply-side factors drove the recent surge in inflation, which peaked in 2022. As these factors have dissipated and consumer demand has weakened, so too has inflation.

YoY Inflation vs. Real YoY PCE Growth by Quarter (%)

Real YoY PCE (Left Axis) vs. YoY Inflation (Right Axis)

On a larger level, the relationship between CPI and real PCE has undergone a major shift beginning in 1980. During the previous 30 years, CPI and PCE growth tended to move in opposite directions. Consumer demand seemed to respond to price changes. In the years since, however, CPI and real PCE growth began to move in tandem. CPI was no longer a driver of consumer spending but was rather driven by it. Even with falling inflation, the consumer did not consume more.

Real YoY-PCE Growth vs YoY NFP Growth by Quarter

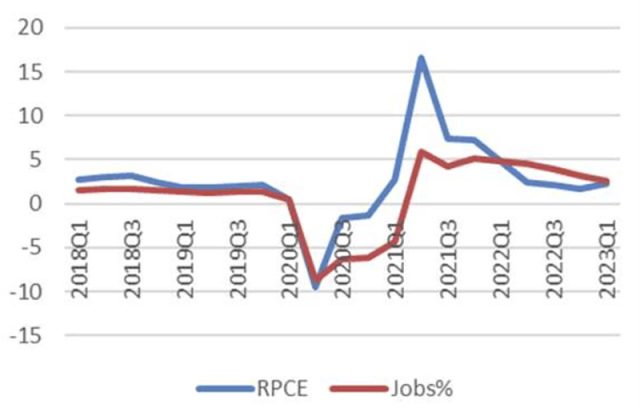

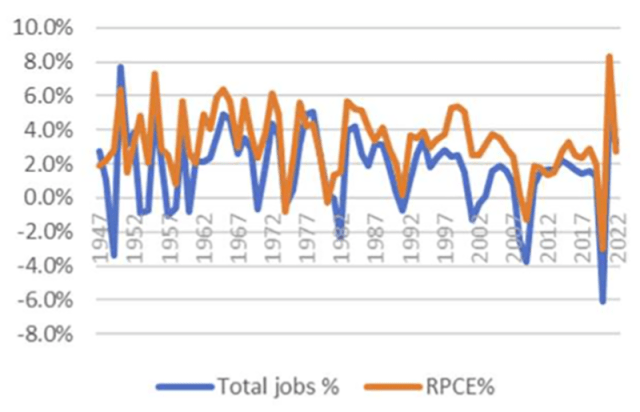

4. Declining Job Growth

Consumer spending drives job creation in a consumer-driven economy. After fluctuating during the pandemic, the rate of job creation has fallen in line with nominal and real PCE growth.

Real YoY PCE vs. YoY Non-Farm Payroll (NFP) Growth

And What about the Long-Term Outlook?

So, what does all this imply about the future of the US consumer and the US economy? There are three implications:

- The consumer’s influence will continue to diminish. Why? Because the headwinds are not expected to ease. And as the consumer falters, GDP growth will likely falter as well, potentially causing a recession.

- The last 15 years demonstrate that increases in PCE growth require additional and ongoing fiscal or monetary support for the consumer. That constitutes our US-Japanification scenario wherein fiscal and monetary authorities assume the debt necessary to keep the economy going.

- This fading consumer trend spans the last several decades and myriad technological advances, the emergence of the digital age, the outsourcing phenomenon, etc. Despite such developments, the basic direction of consumption growth didn’t change. Each new innovation simply shifted expenditures from one sector to another; they didn’t increase total expenditure growth. Why? Because of consumer-funding constraints.

These constraints and how fiscal and monetary policymakers respond to them will define the US economic outlook for the foreseeable future.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Drazen Zigic

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.