Read the complete three-part series.

The European Central Bank (ECB) began buying corporate debt as part of its corporate sector purchase programme (CSPP) in 2016. Given its clear and unambiguous legality, the CSPP could create the expectation among investors of an “ECB put,” that the bank will do “whatever it takes” to provide liquidity and restore order to the financial markets in the event of a crisis. Thus, the program may have a lasting effect on European credit markets.

So, what does the data show? Has the CSPP repriced corporate credit in Europe?

Unlike the Fed, the ECB has confined its corporate sector bond purchases, detailed in the chart below, to investment-grade (IG) debt. While the Fed bought $14 billion in bonds and exchange-traded funds (ETFs) in 2020, the ECB purchased as much in the first two-and-a-half months of the COVID-19 pandemic alone. These purchases accounted for a much higher percentage of the European corporate bond market, which is less than half the size of its US counterpart.

ECB Corporate Bond Purchases: Significant and Persistent

Source: Bloomberg

But if the US experience is any guide, investor perception is influenced not just by the scale of the bond buying but also by how confident market participants are that the central bank will intervene in difficult times.

Option-Adjusted Spreads

The historical option-adjusted spreads (OAS) for European A-rated and BBB-rated corporate debt, visualized below, widened to all-time highs during the global financial crisis (GFC) and widened again during the European sovereign debt crisis in 2011. While the ECB launched support programs to counter the GFC and expanded them to the banking sector amid the sovereign debt crisis, it did not directly buy assets until 2016.

Euro Corporate Option-Adjusted Spreads (OAS)

Source: ICE data

Since then, the 2020 sell-off has been the Fed’s and ECB’s most significant challenge and the first instance where evidence of a central bank put might surface. Like the Fed, the ECB stepped up its asset purchases in response, and credit spreads returned to their pre-COVID-19 levels by year-end 2020.

While crises precipitated by different catalysts don’t make for apples-to-apples comparisons, spreads increased much less during the pandemic than in the two previous sell-offs. Perhaps the ECB and other centrals learned from past experience and took swifter action.

A look at the history of credit spreads before and after the inception of ECB asset purchases shows no conclusive evidence of an “ECB put.” But it does suggest that the market has changed since the ECB first intervened. Median credit spreads for A-rated debt in Europe are in line with pre-CSPP levels, according to the preceding illustration, while spreads for lower-rated BBB debt have narrowed since 2016. Of course, in a lower interest rate environment like that of the last several years, investors’ hunger for yield grows. US credit spreads tell the same story. If there is an expectation that central banks will intervene during crises, greater risk-taking looks “safer.” Yet the lower median for spreads also occurred amid a massive increase in corporate credit issuance and in corporate leverage.

Pandemic Induced Spread Widening More Muted Than Past Crises

2. 4 May 2011―29 November 2011

3. 21 February 2020―3 April 2020

Source: ICE data

Annualized spread volatility, calculated from weekly changes in spreads, is displayed in the graphic that follows. Since the start of the CSPP, spread volatility has decreased. While correlation is not causation, lower spread volatility and lower equilibrium spread levels could signal an implicit ECB put. Though the Fed was also buying debt during this period, its purchases were limited to government bonds and agency mortgage-backed securities (MBS) until the pandemic broke out. While median spread levels have declined in the United States, economic growth was relatively robust as investors pursued riskier assets. The substantial increase in downgrades could explain why BBB spreads exhibited somewhat higher volatility as corporations took advantage of lower yields to lever up their balance sheets.

Credit Spreads Better Behaved in the Presence of ECB Buying?

Sources: : ICE data and MacKay Shields

The corollary to this situation is a central bank put would be expected to mitigate extreme spread widening and lead to lower volatility. The distribution of spreads would then have shorter tails, or at least shorter right tails. The following exhibit bears this out.

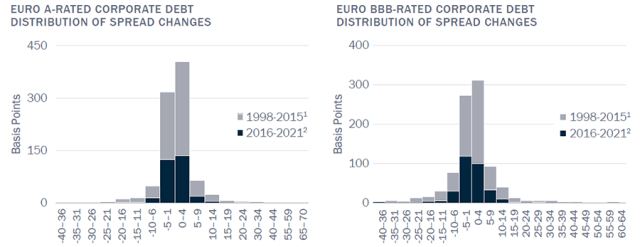

Thinner Tails Exhibited but Dearth of Events Gives Pause

2. January 2016―December 2021

Sources: ICE data and MacKay Shields

Because of the inherent asymmetry of corporate debt, we would anticipate the distribution of weekly spread changes before and after the inception of the CSPP to have a fatter right tail. While there is a fat tail, it is not as pronounced in A-rated debt — though it surely would be in below-IG debt and other markets with higher default risk. The distribution for BBB-rated corporate debt is similar in shape and, given the lower spread volatility, the tails are shorter.

Again, the post-CSPP period is only six years old with fewer extreme events than the 18 years prior. Nevertheless, the modestly tighter spreads, lower spread volatility, and shorter right tail could indicate a central bank put.

Realized Spread Behavior vs. Fair Value Model

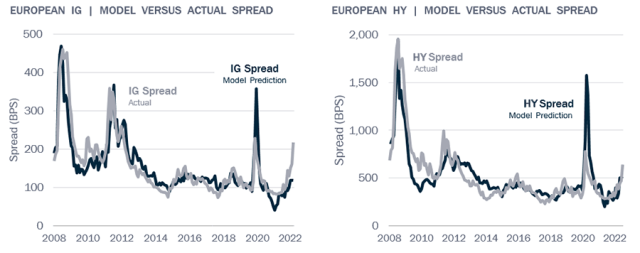

We also looked for evidence of an ECB put by comparing realized spread behavior with several fair value models of corporate spreads published by major investment banks. These models are based on monthly estimates of the fair value of broad-based market spreads and apply a set of sensible factors to estimate the price of credit risk. The UBS model, which we focus on here, uses explanatory variables that capture economic fundamentals, credit performance, and market liquidity measures to estimate the fair level of spreads. Modeled spreads have historically tracked realized spread behavior, as shown in the following illustration.

Spreads Widen by Less Than Expected in 2020

The pandemic sell-off in March 2020 is the first extreme market event since the CSPP’s inception, and according to the model, spreads for European IG debt should have grown by 265 basis points (bps), from 94 bps in early February to almost 360 bps. But they only widened by 135 bps, or about half that amount. Spreads for high-yield debt, which the ECB does not purchase, did not increase as much as the model predicted either.

Of course, these generalized models can’t incorporate every market-moving factor and deviations may occur for countless reasons. For example, the figure above demonstrates that European IG spreads recently grew by more than was forecast. Why? Because of weak economic performance in Europe, an abrupt pullback in quantitative easing (QE) by the ECB, and poorer-than-expected liquidity.

That the spread widened more than expected as the ECB dialed back its stimulus, stopped purchasing new debt, and ceased expanding its balance sheet does not disprove the existence of an ECB put, however. The ECB, like the Fed, has prioritized fighting inflation and appears willing, at least for the moment, to accept slower growth. What the ECB would do if the economy went into a tailspin or financial markets took a nosedive is an open question.

Options Markets

Do the options markets shed any light on a potential central bank put? If investors expect less volatility in the future and smaller losses during times of stress, might they pay less for downside protection?

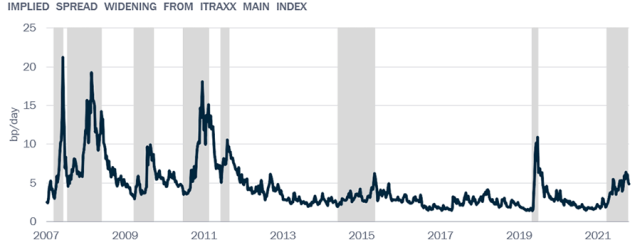

The following figure compares the implied spread widening, in bps per day, of iTraxx Main 3m 25d Payer swaptions with the actual credit spreads of the iTraxx Main index when they grew by more than 50 bps. Protection costs spiked in line with the severity and duration of the widening spreads. In late 2015/early 2016 and again in 2020, the cost of protection did not seem to rise as much as in past crises or in the empirical models detailed above. In late 2015/early 2016, spreads rose more gradually, there wasn’t a sudden market shock, and the volatility spike was less severe. In 2020, spreads increased much more dramatically, began to recover sooner, and downside protection costs declined rapidly.

Even in the current market downturn, which was initially driven by rising interest rates, spread increases were more muted. While recession fears have risen of late, and the Russia–Ukraine war certainly has the potential for surprises, spreads have not widened all that much.

Rise in Cost of Insurance More Muted

Shaded area indicates widening of spreads.

Sources: Bloomberg, Goldman Sachs, and MacKay Shields

So, has a central bank put come to the bond markets? While there are only a few extreme sell-offs on which to test the hypothesis, the limited evidence from Europe indicates it is a possibility. And in the absence of legal or legislative hurdles to further ECB bond market intervention, investors could be forgiven for anticipating such a put.

But the situation in the United States is different. The Fed’s corporate debt repurchase program is newer, and there are barriers to further interventions. Nevertheless, the Fed has opened the door. In the final installment of this series, we will explore whether that has reshaped US bond markets.

Don’t miss the first article in this series.

If you liked this post, don’t forget to subscribe to Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/ ollo

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.