When does a potato cease to be a potato? It’s a question that has plagued some of Britain’s finest legal minds for at least some time this year.

Last January, FT Alphaville treated readers to 3,400 crunchy words on Walkers Snack Foods Ltd v Commissioners for His Majesty’s Revenue and Customs, a First-Tier Tax Tribunal case concerning Walkers’ attempts to get VAT taken off their Sensations Poppadoms products.

HMRC — the UK’s tax authority — had slapped Sensations Poppadoms with a standard 20 per cent duty, on the grounds that they fell within the non-exempt category that includes:

potato crisps, potato sticks, potato puffs, and similar products made from the potato, or from potato flour, or from potato starch

Walkers, attempting to avoid the levy, argued without success that the products were actually more akin to conventional poppadoms, which are zero rated as a foodstuff.

Just over a year after we published, Walkers and HMRC were in court again, with the former appealing the FTT decision in front of the Upper Tribunal. A judgment landed on Friday — did Walkers finally get the run of HMRC, or was the crisps giant left feeling salty?

You say potato, we say warzone

To rapidly summarise a complicated courtroom clash, Walkers tried the following arguments to get Sensations Poppadoms off the VAT hook:

-

They are not ready for human consumption

-

They are not a potato product

-

They don’t *taste* like a potato product

-

They’re not like crisps

-

They’re not like crisps because they’re part of a meal

-

They’re not like crisps because they aren’t packaged like crisps

-

They’re not like crisps because they are called poppadoms

-

They’re not like crisps because they don’t look like crisps

-

They’re not like crisps because they don’t work like crisps

-

They’re not like crisps because they don’t do the same things in your mouth that crisps do

-

They’re not like crisps because the public doesn’t think of them like crisps

-

Taxing Sensations Poppadoms but not conventional poppadoms will distort UK markets

These were duly dismissed by the FTT judges. But Walkers’ barrister Max Schofield (who readers may remember from our coverage of sports drinks and flapjacks) was back and ready for a scrap.

Schofield brought forward eight grounds for appeal, six of which were pursued before the Tribunal (Mr Justice Meade and Judge Ashley Greenbank).

Grab a cup of tea and some standard-rated snacks, and let’s get into it.

Ground 1: Clear as spud

FT Alphaville doesn’t have a Latin speaker on staff, but Reuters Practical Law tells us expressio unius est exclusio alterius means “the expression of one thing is the exclusion of the other”.

So it is, Schofield argued, in the world of potatoes.

Potato snacks of the type Sensations Poppadoms wishes not to be are those “made from the potato, or from potato flour, or from potato starch”, he told the Tribunal, a list that excludes potato granules.

The judgment paraphrases him thusly:

a) The words “the potato” could not be intended to include every ingredient derived from potato – if so, the references to “potato flour” and “potato starch” in excepted item 5 would be redundant.

b) The construction adopted by the FTT also ignored the use of the definite article, “the”, before “potato” in excepted item 5. The words “the potato” properly extended to the use of sliced potato in the manufacture of potato crisps, but could not extend to products made from ingredients derived from potato, such as potato granules, which were pieces of potato that had been cooked and then dried, before being used to create dough pellets, which were then fried.

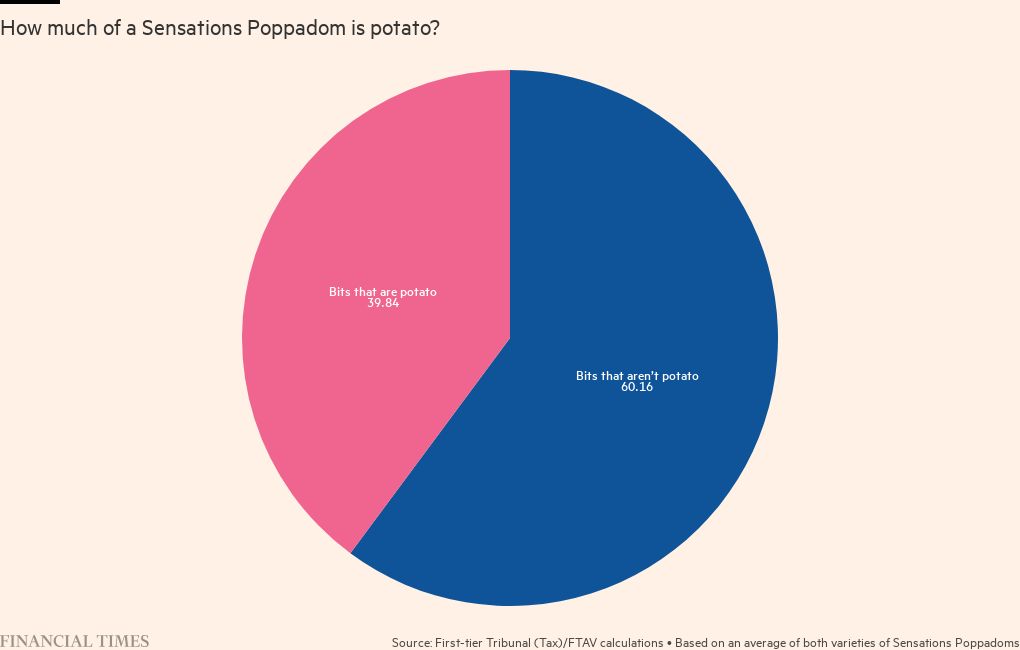

On that basis, the lawyer argued, Sensations Poppadoms could only be seen as 17 to 18 per cent “relevant” potato content — the starchy bits.

This, HMRC argued, was unreasonable. “The potato”, said its counsel Giselle McGowan, was a term wide enough to include potato granules. Indeed, their inclusion within the broad term was intentional, she suggested.

The Tribunal sided with HMRC.

“Mr Schofield’s argument suggests,” they write:

. . . that there is a point in a manufacturing process at which ingredients derived from potato cease to fall within the term “the potato” and so fall outside excepted item 5 unless they are potato flour or potato starch. Even if that is correct . . . the dividing line is primarily a question of fact and degree for the FTT as the factfinding tribunal. Unless the FTT has adopted “an untenable interpretation of the legislation or a plain misapplication of the law to the facts”, its decision on that issue ought not to be disturbed on appeal.

That being said, they didn’t love the suggestion by McGowan that the phrase should encompass all potato-based content.

As the Judgment rather succinctly put it.

We heard full argument on this point

The problem here is somewhat theological: at what level of transformation does a potato cease to be a potato? Is the point of no return linguistic? Or is it physical? It’s a bit like Theseus’s Paradox, albeit with less replacement and more starch.

Faced with these difficult questions, the Tribunal understandably ducked:

Before leaving this ground of appeal, we should acknowledge that we have only summarized the submissions made by the parties on the question of statutory construction, which went into some detail as to the canons of construction and interpretative factors that should be applied . . . the question for the tribunal is a short practical question calling for a short practical answer

An epistemological crisis was averted, and ground 1 was dismissed.

Ground 2: Tater made?

Naturally, there was still scope for debate. OK, perhaps potato granules can be considered derivative of the potato — but is there sufficient “qualifying” potato in a Sensations Poppadom?

As Schofield presented it, the 17 to 18 per cent of any given Sensations Poppadom that is potato starch represented a materially small element of the overall product.

Of relevance here is United Biscuits (UK) Limited v HMRC [2011], in which a first-tier tax tribunal decided that “Discos” and “New Recipe Frisps” — with potato content of about 27 per cent each — were not “from the potato”.

The Upper Tribunal — having already determined potato granules to be part of the extended potato universe — didn’t like this line of argument, judging that the potato starch and granules must be combined to judge overall potatitude. Which gives us another chance to crack out our advanced dataviz from last year:

In fact, the Tribunal seemed keen to distance itself from the United Biscuit decision:

while there clearly has to be some potato content for a product to be properly described as “made from” the potato, potato flour or potato starch, there is no justification for a test that relies on a particular level of potato content.

Also brought up in discussion was a case we’ve previously covered concerning the humble Pringle, Revenue & Customs v Procter & Gamble UK (2009). In that case, judges:

dismissed arguments that a product had to have an “essence of potato” or “quality of potatoness”

On that basis, the Tribunal concluded the FTT had acted fairly, and dismissed ground 2.

Grounds 4, 5, 6 and 8: Max vs factors

With Ground 3 unpursued, the pace picked up.

The remaining grounds all concerned the multifactorial assessment undertaken by the FTT, in which it considered the nature and presentation of the Sensations Poppadom across a variety of contexts and vectors.

Ground 4 falls within the “They’re not like crisps because they are called poppadoms” category, and produced arguably the spiciest part of this hearing.

In the FTT hearing, Walkers had argued that the name “Sensations Poppadoms” clearly distinguished its products from, from instance, “potato crisps”. As the FTT memorably wrote then:

Nominative determinism is not a characteristic of snack foods: calling a snack food “Hula Hoops” does not mean that one could twirl that product around one’s midriff, nor is “Monster Munch” generally reserved as a food for monsters.

It was an entertaining but odd argument at the time, and Schofield was keen to dwell on that oddness:

He argued that the FTT’s approach – refusing to give any weight to the name given to the product – confused the brand name of a product with the “legal name”, “customary name” or “descriptive name” of a product, one of which was required to be included on the packaging under food labelling rules.

As a result, weight should properly have been given to the use of “poppadom” in the products’ names.

McGowan, arguing against this, suggested the FTT had simply concluded that the name was irrelevant.

In this matter, the Upper Tribunal had some sympathy for Walkers:

we acknowledge Mr Schofield’s criticisms of the FTT’s references to “Hula Hoops” and “Monster Munch”. They are brand names and clearly of no relevance to the multifactorial assessment. We agree with him that the FTT appears to have treated the reference to “Poppadoms” in the labelling of the product as a brand or trade name rather than as a customary name…

We have expressed some reservations about the FTT’s approach to some aspects of the multifactorial assessment – in particular, the reasons that it gave for not affording any weight to the name or description of the products

The problem, they argue, is that the FTT wasn’t trying to figure out whether Sensations Poppadoms are poppadoms, only whether they are similar to potato crisps:

In that context, the customary name of a product is of limited relevance. The fact that a product might customarily be called a “poppadom” does not in principle prevent it from also being similar to a potato crisp.

Ground 5 was all about flavours, ie the “They’re not like crisps because they don’t do the same things in your mouth that crisps do” challenge.

At the FTT, Walkers had argued that the flavours of Sensation Poppadom available — Lime & Coriander Chutney, and Mango & Red Chilli Chutney — were distinct from conventional potato chip flavours.

The judges in that instance didn’t bite (the argument, at least), positing that no flavour was truly distinct in a world with crisp varieties “as diverse as hedgehog, haggis, sweet chilli, sour cream, and ‘cheese & port’”.

That, the Upper Tribunal agreed, “was not an unreasonable conclusion for the FTT to reach”.

Ground 6 was the gram flour round. At the FTT, the judges had determined through careful research (aka eating) that the Sensation Poppadoms’ potato content helped mask the flavour of the gram flour present in the products — but declined to recognise that flour as a distinct feature, given its taste was masked by flavourings.

Schofield argued this had been an error by the FTT — who had, in the judgment’s phrasing of his argument — “conflated the ingredients with their taste”.

Again, McGowan characterised this as a case of the FTT simply avoiding distraction from the task at hand. And the Upper Tribunal agreed, concluding that the FTT had been correct to assess texture and flavour as potentially differentiating features, rather than treat gram flour as an inherently transformative component (like putting a Mentos in a bottle of Diet Coke, maybe).

Ground 7 was skipped, meaning Ground 8 was Walkers’ last stand. Judgment:

In relation to the final ground of appeal (Ground 8), Mr Schofield said that throughout the FTT Decision, the FTT failed to appreciate that poppadoms were a “conceptually distinct and recognized non-crisp product”. The typical consumer would understand that a poppadom was a fundamentally different product from a potato crisp.

To back up this argument, Schofield once again presented the survey findings that had been thoroughly rinsed by the FTT.

The survey, “he asserted”, showed:

that the majority of consumers would choose other poppadoms as a replacement product if Sensations Poppadoms were not available

Indeed, the survey — conducted by PepsiCo, who own Walkers — did find 58 per cent of respondents would consider buying “any poppadoms” if Sensations Poppadoms were unavailable.

Unfortunately, as the FTT noted, the results also showed 84 per cent of those same respondents would consider buying “some form of potato crisp” instead.

Rather than simply re-roasting PepsiCo’s research, the Upper Tribunal took a simpler view: once again, this was all irrelevant in the context:

the question is not whether the products are similar to poppadoms, it is whether they are similar to potato crisps. The products may be similar to poppadoms, but that does not prevent them from being similar to potato crisps

Conclusion: Packet in

It will not surprise readers to learn that Walkers was not successful, its appeal dismissed.

The Tribunal was tasked, in its own words, to determine:

is whether the FTT reached a conclusion, which is so unreasonable that no reasonable tribunal, properly construing the statute, could reach

The answer to that was a firm no, despite certain reservations:

The FTT failed to recognize that the descriptions of the products as “poppadoms” and “potato and gram flour snacks” were not at an equivalent level to the brand names and trade names to which it referred. However, even if it had done so, it would not, for the reasons that we have given, have materially affected the overall assessment; it was a very minor part of the overall picture.

It’s been almost 500 years since Juliet first leaned over a balcony, and asked the night air: “What’s in a name?”

Finally, in the case of potato snacks, we have an answer: not much.