I am going to try and explain a little subtle difference between phrases that I use when I engage in income planning with the community.

Perhaps I will also explain a few more since this article is going to be very short.

- Income requirement: When you are planning your income stream before you need for a certain purpose how much you need.

- Income needs: Same as income requirement.

- Spending/Expenses: How much you actually spend today or how much you intend to spend in the future as you live your life.

- Recommended Income: An income that is recommended for you to spend, in a given year, based on how we design the income system, to which the investment portfolio is part of.

Suppose I spend $25,340 on average for the past 3 years. That is what I keep track of in my budgeting and what I can observe.

My Income Requirements/needs can be a future-inflation-adjusted $30,000 yearly if I were to plan for my financial independence in ___ years.

This is because I have some conservatism that I would like in the income stream I eventually get.

I can also have Income Requirements need to be a future-inflation-adjusted $20,000 yearly.

Why?

Perhaps I reflect upon my spending and wish for the income stream to only cater for a specific 4 spending line items instead of all line items.

That is also quite sound if you understand what you are planning for.

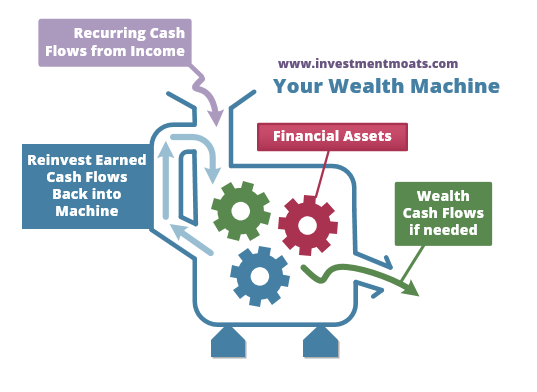

Trying to construct a wealth machine is concept that I often talked about in the past. The idea is to create a portfolio, partially manage by yourself and other that can grow your wealth in a manner that is long term sustainable. You will inject capital periodically. Anytime there is sells and dividends, that gets circulated back into the system.

The important thing is you determine when, how much to spend from this machine depending on what is your objective.

The actual income that gets out of that, or what you withdraw is an actual spending. This means that if you decide to withdraw monthly, and you withdraw $1,200 from your Wealth Machine, that is your spending.

So what is Recommended Income?

In a wealth machine, meant more for income, something like my Daedalus Income Portfolio, you may wish to plan how much income you wish to periodically get out from the machine, how periodic, do you inflation adjust or not, or do you reduce the income.

I would view the eventual income as the Recommended Income.

Suppose in my case, Daedalus is plan to pay for my inflexible spending needs for a long time say a tenure of 60 years or more. I prefer to design an income system that is battle-tested to give an inflation-adjusted income in the worst historical scenario.

So I plan to spend from Daedalus based on an initial 2% Safe Withdrawal Rate. (You can read about the safe withdrawal rate methodology here: Why the Safe Withdrawal Rate (SWR) is Essential for Your Financial Independence)

So if the portfolio value is $1,500,000 today, then the starting income is $1.5 mil x 0.02 = $30,000 yearly or $2,500 monthly.

The $30,000 yearly is the recommended income for the first year.

Now a 2% Safe Withdrawal Rate is an income system where you adjust your income based on the previous year’s spending by the prevailing inflation rate.

So say for the past 3 years the inflation rate from consumer price index is like this:

- -3%

- 5%

- 7%

The recommended income from Daedalus based on the CPI for each of the year is like this:

- Year 1: $30,000

- Year 2: $30,000 x (1+ -0.03) = $29,100

- Year 3: $29,100 x (1+ 0.05) = $30,555

- Year 4: $30,555 x (1+ 0.07) = $32,693

In this way, the system plan for an income stream that adjusts for inflation. It also provide income consistency in an inflation-adjusted manner.

So the recommended income at the start of the fourth year is $32,693.

If I spend $26,000 only, that is my actual spending/expenses.

Can I spend less than $32,693? Yes, because this amount is a recommended income if we believe in the system and wish for Daedalus to provide the income as it should.

Now can I spend $60,000 instead of $32,693 for the fourth year?

Yes.

However, I will have to understand the implications. Spending $60,000 or $26,000 is not the recommended amount. $26,000 is safe because that is lesser than the recommended amount but $60,000 is more.

However, because I am so familiar with the Safe Withdrawal Rate and I know that starting with a 2% is on a very conservative side and even if the $60,000 is now 3.7% based on my current portfolio value is conservative, it would not jeopardize the longevity of Daedalus.

The critical thing is whether you know what you are doing.

Same $1,500,000 but Based On a Different Spending System

Now I could design Daedalus spending system differently.

Instead of a 2% initial Safe Withdrawal Rate, I can design Daedalus to be based on a recommended income of 5% of the prevailing portfolio value.

The investments is the same. Currently, it is a portfolio equity and fixed income ETFs in a 85% equity 15% fixed income mix.

For example, suppose for the past 3 years the growth of Daedalus is like this:

- Year 1: +15%

- Year 2: -45%

- Year 3: +50%

If our planning at the start is 5% of the portfolio value, then the first year recommended income that we can withdrew at the start is $75,000.

Now at the start of second year, the recommended income would be (($1,500,000 -$75000) x 1.15) x 0.05 = $81,937.

At the start of third year, the recommended income would be (($1,638750 – $81,937) x 0.55) x 0.05 = $42,812.

At the start of forth year, the recommended income would be (($856,247 – $42,812) x 1.5) x 0.05 = $61,007.

Hey Kyith, isn’t the income a bit too volatile?

Well, you are the one that designed it.

Some folks like this percentage of prevailing portfolio strategy, but partly it is also because of the return numbers I use. If your portfolio is less volatile, using such a strategy would create a less volatile income.

The recommended income does not measure up closer to inflation yearly because this income stream is based on market conditions.

We will often say that this income strategy is meant more for flexible income goals such as discretionary spending.

Recommended Income Allows You to Detach Your Income Planning From Your Actual Spending Today, to Focus More On the Nature of Income You Want.

Too often, we plan based on what we spend today.

This is not too wrong, especially if someone tracks the spending.

But sometimes you might want to plan for a medical sinking fund for your spending on your annual shield and rider premiums. That is just two spending line items.

Do you plan using all your current spending of $87,000 yearly?

Cannot be right.

Using recommended income in small ways forces you to confront what sort of income you need. And in this case we know that the premiums go up by age, but also go up by non-guarantee insurer adjustments.

So the Wealth Machine, and the income system within, needs to give you a recommended income that address this needs well.

The Wealth Machine and its Income System Concept Detach Your Income planning from the Natural Income Your Investments Provide.

Too often, investors choose their investments based on whether there is a natural income such as interest, dividends from their securities.

Due to their greed, or their high lifestyle desire, they may chase for investments such as YieldMAX funds, options writing strategy, high dividend individual stocks that have high natural income.

When I design Daedalus, it is meant as a potential high yield income strategy. The investments in the portfolio, if they hit median or optimistic returns, can allow me to spend 8-10% initial from $1,500,000 if inflation is reasonable with no problems.

And all the ETFs are accumulating funds which means they don’t give natural income.

High income does not always come from investments from high natural income.

And many struggle to see it. Perhaps it is a psychological thing.

I start off with 2%, because the future is unknowable and we are doing forward planning, on a financial goal that we don’t want it to fail. If you are the kind that are so happy to stop work, then 10 years later can come out to find work when markets are so bad, you use very optimistic recommended income assumptions, then you can start with 8-10%.

But I use 2%, based on my research and my comfort zone.

In a way, I detach the planning from the natural income of the investments.

This will force you to consider if you aren’t constrain by natural income, then what would you invest in.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

Advances While Market Declines: Some Information for Investors")

Q2 2026 Earnings Call Transcript")