Two members of my Singapore Financial Independence Telegram group contributed their rules of thumb in managing their portfolios.

We were having deeper discussion about different way risks are perceived.

My member James was giving some reasons why out of the three Singapore banks (UOB, OCBC, DBS), he ended up avoiding DBS and UOB:

“During the subprime crisis, DBS got hit with 2.4 billion while OCBC got hit with 1.3 billion. UOB got round the crisis relatively unscathed.”

My first personal thought is how significant are these 2.4 and 1.3 billion for each company. If we look at these companies from the system perspective, should blame or judge them as poor risk management or did you forgot that they know parts of these financing deals they make will fail and design & implement a system to manage that.

I think is both.

- There should be some conservatism if we practice our critical thinking. Which means we should not make some of these deals.

- It makes more sound sense to expect different degree of deal failure and design a system for this.

I pushed James to consider that if we are trying to be conservative, and cover all our bases, we are going to leave a lot of deals on the table. Even if we try to cover all our basis by sensing the motivation of the owner and observing the style of management, through their actions, it might be futile because the “base rate” might be generally more management and businesses are problematic. If that is the case, a business is more likely to fail in the long term than succeed.

A good example of acknowledging the base rate of failure but still taking risk are systematic passive or active strategies like Amundi Index tracking funds or Dimensional funds.

- Companies that are weaker don’t impair your entire net wealth.

- Companies that show market-risk, value, profitability, momentum, illiquidity, low volatility premiums have the premiums harvested systematically.

- There are periodic ways to reconstitute the portfolio which means the failures get systematic weed out into the portfolio.

- Different strategies involve equal-weighting, value-weighting, dividend-weighting, which systematically shifts the nature of the portfolio.

All of this work on the base rate that companies generally fail, and we generally don’t know which companies will succeed in the long run.

Sometimes it might be that I am digging up something to argue but I generally think some members like James may glean something from these different perspectives. Both of us probably came from the same world of “only having a few eggs in the basket and bloody watching over that basket like a hawk”. But I think it is important to consider what are we most afraid of, how we protect ourselves in the past, what are other ways that attempt to protect what we are most afraid of and why would they work.

My friend STE shared this extract from a book:

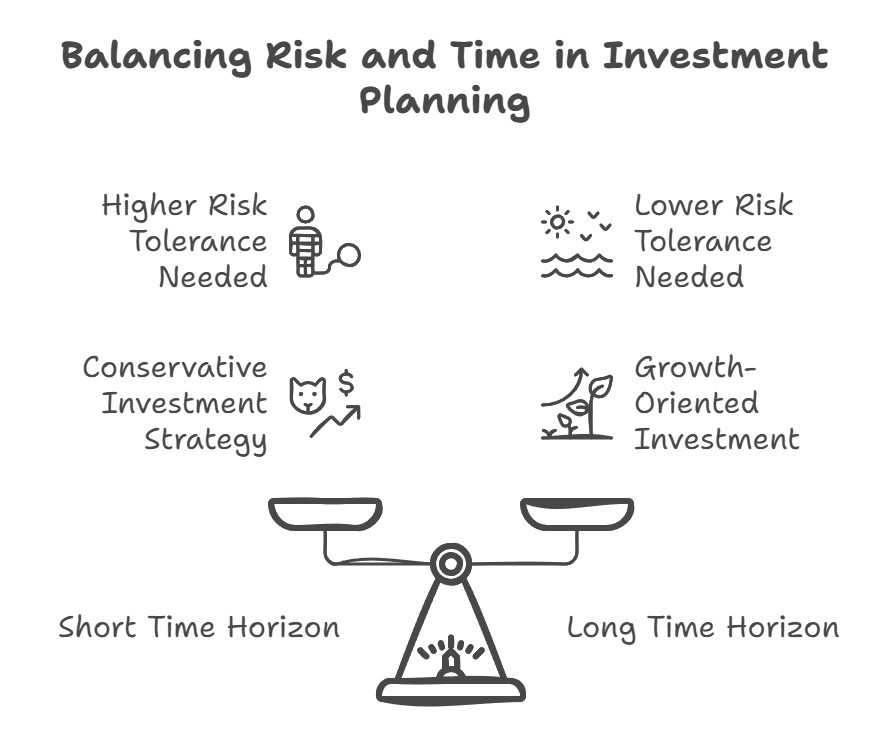

There seem to be two parts, but essentially talking about the relationship between risk and time horizon. It also fills in how net wealth affect how you look at risk.

In planning for the wealth of low net wealth or high net wealth, we kind of first look at the time horizon. The time horizon is how long before you need to use the money. The money for a certain goal. If your time horizon is short, you need the money soon, you cannot hope for much variability in the outcome from your target.

Variability in the outcome of your target is basically risk.

We learn that in various things. The target outcome of flying the plane is to reach Taiwan. The risk is the plane reaches the middle of the ocean. There is a variability in the outcome.

If your time horizon is long, then you have time for your investments to work itself through the various short business cycles so as to properly price the business growth. This means some investments are very challenging if you need the money within 15 years.

We are fxxking scared about a lot of things because we grew anxious if we can have that return, to achieve our goal in time. But many disrespect the importance of the period you need for the investment to mature.

Investors know that if a fixed income doesn’t default, you get back your principle if it matures in X years. Perhaps you should look at equities this way. It is like a 15-25 year pseudo-fixed income. If your goal is less than that, don’t blame us, don’t blame equities for not giving you what you want. You over-expected it. If you are lucky, you can get the outcome. But if you are unlucky…. don’t blame the equities, don’t blame the gurus.

I think what Morgan Housel wrote is damn profound:

“The most important question to ask when thinking about risk isn’t how much volatility or upside you are looking for, but how much time your emotions and goals need for that volatility to play out.”

Whenever we consider an investment, the first question is often how much return we could potentially get. Not many would ask about the experience that we might have to go through to earn that return.

I think many understand that they won’t smuggle drugs even if the returns are worth it because they get the worst case risk they might get into. But we won’t readily consider the experience first. This is because not many tell you that you need 15-25 years. If you know, then would you consider how uncomfortable you would feel?

Perhaps.

Two Asset Allocation Non-Negotiables to Avoid Your Family Dying Poor.

James and another member Lim Der Shing commented on some portfolio guidelines they set so that they don’t fxxk themselves up with concentrated single stock position.

Der Shing’s 2 Bite Size Rules:

- I will put at most 5-6% of my equity portfolio into one company on cost basis.

- A single stock is allowed to grow up to 15-20% of equity total. Then it must be trimmed.

Single stock means a single company risk like Sea Ltd, Ali Baba, Beike or DBS etc. Firms like Berkshire Hathaway does not count.

James:

- 10% max per company.

- He doesn’t trim

- Since his biggest exposure is properties in Singapore, that forms a big chunk of his investments.

I should contextualize that both are referring to wealth that has already built up, and what they produce in work income is miniscule compare to the portfolio. We are talking about north of eight figures here. What Der Shing and James are afraid of, can be different from someone with a work income coming in or in the process of building up their wealth.

I think James does trim, it is just that he doesn’t remember because we have seen examples of that. Selling away is in a way trimming. I guess some can take a step back and be more structured in the way they think. Read in a different way, equities form a much smaller portion of James’ portfolio that even if 10% is pretty concentrated, that equity holding is still pretty small in the grand scheme of the entire portfolio.

Limiting your portfolio to a smaller amount is more about playing defense first. In 2021, I wrote on Providend about two illuminating questions that we can ask ourselves with an investment decision we are about to make.

The first question might fit more here. There are two ways of phrasing the same question:

- I know in this uncertain world, no one can predict that the likelihood of mistakes will go up, no one wants to make a mistake but which mistake can I least afford to make?

- After going through 2008, we know that most mistakes are recoverable but what are the mistakes that I do not wish to make?

This questions force us to think about our investments with how deep the risks we can see (and also cannot see) and relate to how important is our financial goal.

If you think that you have enough money for your lifestyle, would you still put 30% in a single stock, single sector, a product of concentrated risks?

I still see this kind of behavior around.

They have immense trust in:

- Their ability to be nimble.

- That their concentrated position would have positive sequences of outcome from year 1 till year 30.

- Don’t know what kind of weird logic.

I think people failed to grasp the “base rate” here and generally plan with optimism even though they think their plan is conservative.

Or that there are people who technically have enough money trying their best for their family to die poor.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

")