In the dog days of summer, the nearest you might get to an adrenaline rush is when you click on a square in Minesweeper and see a surprising number of blocks suddenly free up. But this kind of cascade has an interesting analogy in financial market crises.

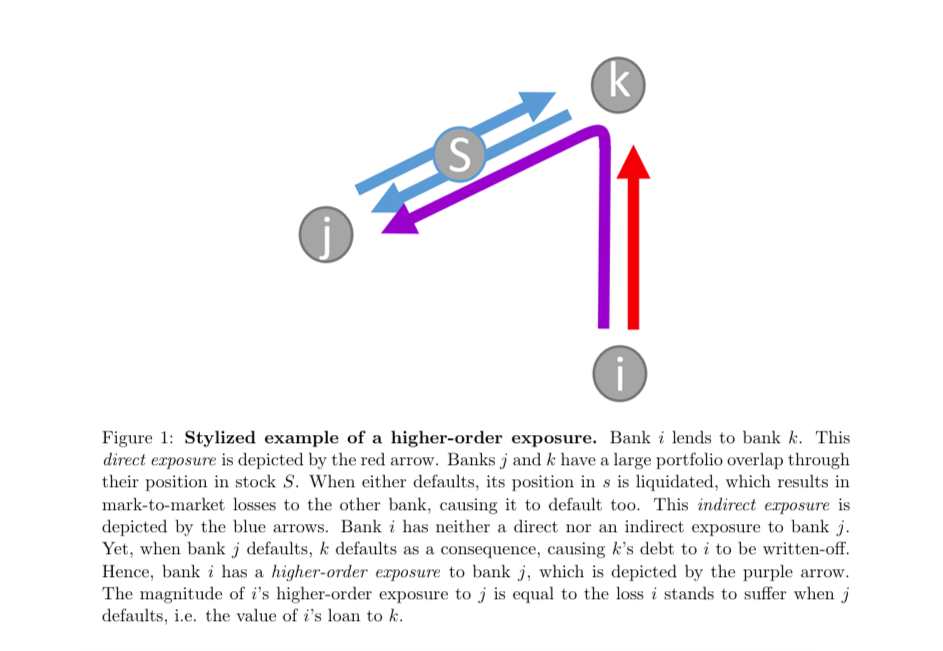

As well as the immediately adjacent pattern of exposures, it’s been known for a while that banks and shadow banks can be brought down by “indirect” exposures. Whether or not you’ve directly lent to a counterparty, if that counterparty has a similar portfolio to you, then you’re at risk. If they get into trouble they could try to liquidate their holdings in a fire sale, driving the price down and potentially wiping you out with mark-to-market losses.

This is one of the reasons why financial regulators have been getting increasingly concerned about the lack of information about “crowded trades” and about banks’ ability to manage counterparty exposures.

After all this is what caused Credit Suisse so much trouble after the collapse of Archegos, and arguably started its death spiral. There was even a proposal last year that hedge funds should be required to give their prime brokers complete visibility of all their trading books, although in the end it got dropped.

However, a big problem is that direct and indirect exposures are by no means the only kinds of linkage in a real crisis.

What if you have no exposure to a counterparty and no portfolio overlaps, but that counterparty is in a separate crowded trade, with somebody else that you do have exposure to? Your own capital could be at risk from what happens to someone that you don’t even know you’re exposed to. This sort of thing is called a “higher order exposure”.

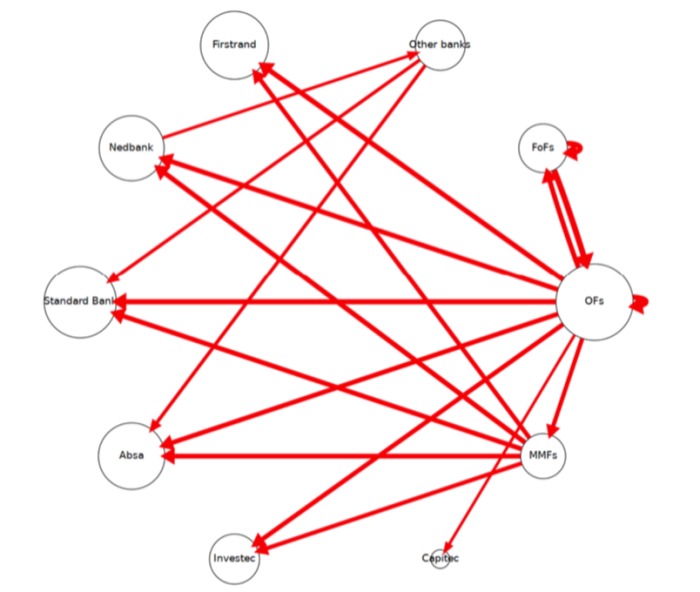

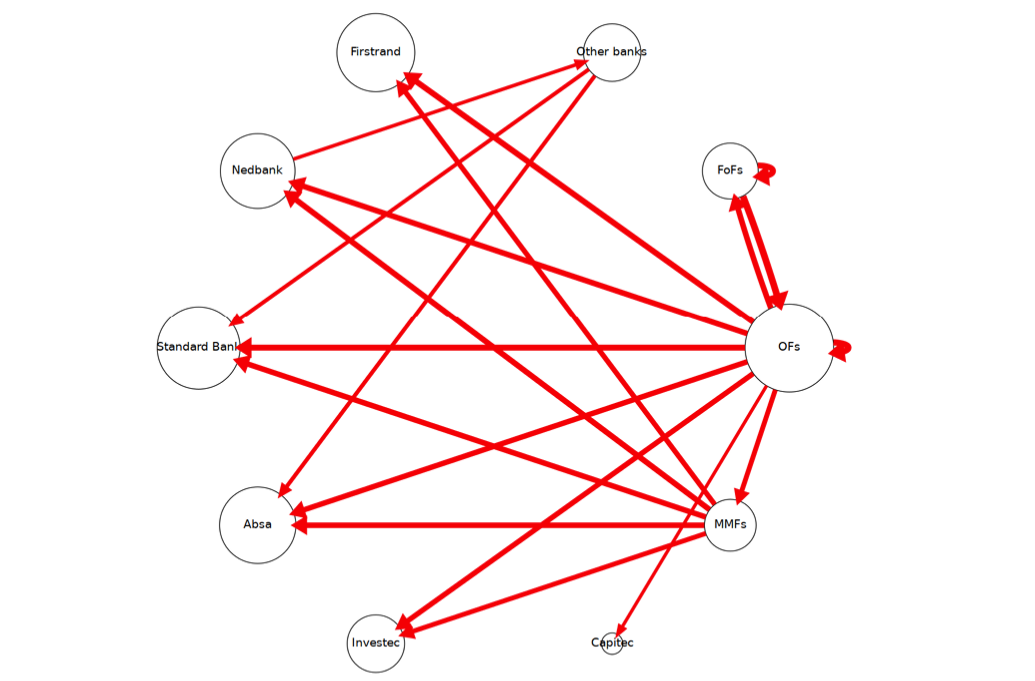

The diagram above comes from a recent working paper from the ECB research department, where they try to find out how much these higher order exposures matter.

They use data from the South African debt and equity markets. That’s because they are reasonably deep and liquid but also relatively small and insular, so it’s possible to get comprehensive coverage of who is exposed to which securities.

It lets you draw cool graphs like this one (zoomable version):

Because they had full data on securities holdings, the ECB researchers were able to calculate the higher order exposures between the South African banks — five layers deep.

So, say, although Absa’s direct interbank exposure to Capitec might be small, when you take into account the possibility that financial distress at Capitec might cause it to liquidate a portfolio which imposed losses on a hedge fund, which was held by a fund of funds, which consequently had to liquidate a portfolio which overlapped with a money market mutual fund which Absa was lending to . . . the true exposure might be quite substantial.

In fact, the ECB researchers — Garbrand Wiersema, Alissa Kleinnijenhuis, Esti Kemp and Thom Wetzer — found that “higher-order exposures” often accounted for more than half of the total, and that this proportion tended to be higher during financial crises.

It’s just like a game of Minesweeper, when your careful deduction and analysis is often less important than the number of blocks that happen to get cleared away because of random structures that you had no way of knowing about.

This is bad news, because it confirms the most pessimistic suspicions possible.

Everyone who has lived through a financial crisis knows that higher-order exposures exist and matter. They are, in many ways, what distinguishes a genuine crisis from a normal screw-up, because they create that atmosphere of everything going wrong at once, and even the good banks still getting hit.

But quantifying their importance in this way makes it clear that it’s almost impossible to do anything about them. If you can’t really know your true underlying exposures without knowing the entire pattern of lending and securities holdings for the entire system, then realistically you can’t know them at all. And if it’s unrealistic in South Africa then it is fantastical in bigger or more connected markets.

The ECB researchers therefore argue that capital requirements should be recalibrated to take account of higher order exposures:

To better protect financial stability, regulators should incorporate higher-order exposures into their risk assessments and regulatory frameworks. This requires collecting more detailed, granular data across a wide range of financial institutions and using models that capture the complex, multi-layered network of financial interconnections.

While this study focuses on South Africa, the concept and its policy relevance apply broadly to other financial systems, including the euro area.

However, this doesn’t seem realistic. As well as breaking the link between a capital requirement and the institution’s own business, it would be much more demanding in terms of supervisory data than anything that’s likely to be imposed in the foreseeable future.

More practically, they make a good case for saying that higher-order effects should be taken into account in stress tests, and in decisions about whether to deal with a troubled bank under the insolvency framework or by a Credit Suisse-style bail-in.

For stress tests to fulfil their basic function of assessing exposure and institutions resilience to risk, capturing higher-order exposures is essential. To be able to do that, stress test models should include multiple interacting contagion channels and be designed to study system-wide dynamics, because those elements drive higher-order exposures.

We have demonstrated that compensating for the lack of explicit system-wide models with direct loss multipliers is inadequate as it gives distorted outcomes. To better assess the resilience of financial institutions, stress tests should thus not only measure the capital impact of asset losses from direct exposures, but also from indirect and higher-order exposures.

But maybe the real conclusion ought to be the one that central bank researchers can’t say out loud unless they’re very secure in their job position: the evidence about higher order exposures is a really strong case for not having a crisis in the first place.

Their work is based on the assumption that when a bank or shadow bank gets into trouble, it will have to liquidate its securities portfolio in a fire-sale, pushing prices down below fair value and causing big knock-on mark-to-market losses for everyone else.

But that’s not a fact of nature like the law of gravity; it’s a policy decision.

There might even be a policy trilemma lurking here, allowing you to pick no more than two out of “no bailouts”; “mark-to-market accounting”; and “financial stability”.

What the ECB team have actually discovered is that in a financial system based on mark-to-market accounting, there is a very strong case for “Lombard Street 2.0” — the new doctrine set out in an obscure policy paper of 2022, and operationalised a few times since — that dictates the central bank ought to use its balance sheet to make sure that these Minesweeper-like cascades don’t have to happen.

‘Biggest Risk’ – ‘Siri is a Mess’")

{kind=link}

{kind=link}