Pim van Vliet, PhD, is the author of High Returns from Low Risk: A Remarkable Stock Market Paradox, with Jan de Koning.

High inflation and expensive equities lead to a negative risk-return relationship and shrink the equity premium to zero. In years following this “everything expensive” scenario, low-volatility, quality, value, and momentum factors yield sizeable positive premiums.

Given today’s market dynamics, investors should avoid high-volatility stocks or hope for a different outcome than the historical reality illustrated in this blog post. I will demonstrate that, while the immediate future may not be promising for the equity premium, it looks bright for factor premiums.

Money Illusion

Money illusion means that investors fail to take inflation into account. It is a cognitive bias that makes it difficult to switch from nominal to real returns, especially when inflation is 3% or higher. A study by Cohen, Polk, and Vuolteenaho (2004) on inflation and the risk-return relationship remains relevant today. They use Gordon’s Growth Model, where an asset price is determined by G, the growth rate of future earnings, and R, the discount rate:

Price = G / R

They cite money illusion – the theory that investors discount real earnings with nominal rates rather than real rates. An example is the widely used “Fed model,” where a real stock earnings yield is compared with a nominal bond yield. Asness (2003) criticizes the Fed model. Academically, this is known as the Modigliani-Cohn inflation illusion hypothesis. And it leads to market mispricing, causing the empirical risk-return relationship to flatten. The figure from their paper, “Money Illusion in the Stock Market,” empirically supports their hypothesis.

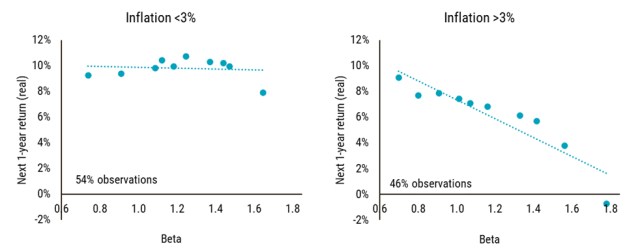

Exhibit 1.

Source: Cohen, Polk, and Vuolteenaho (2004). Annualized returns on vertical-axis and betas on horizontal-axis.

When inflation is low, the risk-return relationship is positive, but it turns negative when inflation is high. This explains the capital asset pricing model’s (CAPM’s) poor performance during high inflation periods like the 1950s and 1980s and it supports the Modigliani-Cohn inflation illusion hypothesis.

Inflation: First Nail in the CAPM’s Coffin

It has been 20 years since the Cohen et al. (2004) CAPM study was published, and US inflation has been above 3% for the past couple of years. Therefore, it is an opportune moment to update and verify these earlier results. We focus on predictive relationships, rather than contemporaneous ones, to provide practical insights for investment decisions.

Using data for 10 portfolios sorted by volatility, going back to 1929 from paradoxinvesting.com, we can test how the CAPM relationship holds in different inflationary regimes. We split the sample into two parts using rolling one-year CPI with 3% as the threshold and consider the next one-year real returns.

Exhibit 2.

Source: Paradoxinvesting

Using this extended database, we can confirm that the cross-sectional risk-return relationship is negative in periods following periods when inflation is above 3%. The relationship is not exactly linearly negative. Rather, it is at first slightly positive before becoming downward sloping for higher-beta stocks.

Valuation: Second Nail in the CAPM’s Coffin

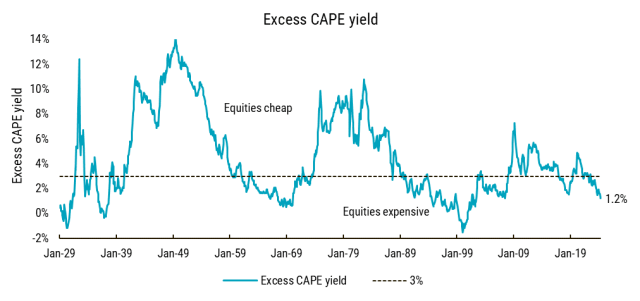

In 2024, the Cyclically Adjusted Price Earnings (CAPE) ratio for the US reached 33, nearing the historical peaks seen in 1929 and 1999. The reciprocal of this measure, the equity yield, stands at 3.0%. With the real 10-year bond yield currently at 1.8%, the excess CAPE yield is 1.2%. This metric is free from the Fed model’s money illusion.

Exhibit 3.

Source: Robert Shiller Online Data

In March 2009, the excess yield was 7.8%, marking the start of a prolonged bull market. Today’s value is much lower than in 2009 and has fallen below the historical median of 3.3%. This low CAPE yield suggests that equities are expensive and expected returns are extremely low. In addition, risk is higher when equity yields are low, as I explain in my 2021 paper.

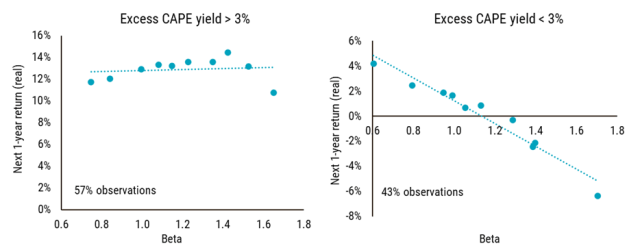

How does the CAPM relationship hold in years following high and low equity yields? The two graphs in Exhibit 4 illustrate the risk-return relationship when the excess CAPE yield is above 3% (“equities cheap”) and below 3% (“equities expensive”).

Exhibit 4.

Source: Paradoxinvesting

High-risk stocks perform poorly in low-return environments that follow expensive markets (low excess CAPE yield). This relationship is stronger and more inverse than during periods of inflation above 3%. After inflation, valuation is the second nail in the CAPM’s coffin. Investors should either hope for a different outcome this time or avoid high-volatility stocks.

Factor Performance in a Low-Return World

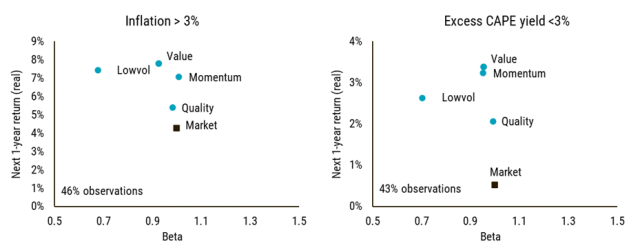

If inflation and valuation have indeed undermined the CAPM — resulting in a negative risk-return relationship — it becomes interesting to evaluate the performance of value, quality, and momentum factor strategies. To do this, we supplement our data with data from Kenneth French. We consider long-only strategies with similar turnover, focusing on the top-quintile portfolios for low-volatility, value, and quality, and the top-half portfolio for momentum.

Quality is defined as operational profitability and backfilled with the market portfolio. Value is defined by the price-to-earnings (P/E) ratio and backfilled with the market portfolio. Momentum is defined by 12 minus one month returns, and Lowvol is defined by three-year volatility. We analyze periods following 1) inflation above 3% and 2) the excess CAPE yield below 3%. These regimes have historically low overlap (-0.1 correlation) and both characterize today’s market environment.

Exhibit 5.

Sources: Kenneth R. French Data Library and Paradoxinvesting

In the year following periods where inflation exceeds 3%, all factor premiums are positive, contributing about 3% to the equity premium. This aligns with a recent study in the Financial Analysts Journal, which shows that factor premiums — including low-risk, value, momentum, and quality — are positive and significant during high-inflation periods. In addition, in the year following expensive equity markets (excess CAPE yield <3%), the real equity return was a meager 0.5%, while strategies focused on low-risk, value, momentum, and quality still provided positive returns.

When these two regimes are combined — representing 17% of the observations — the equity premium turns negative. However, all factor strategies continue to offer positive returns, averaging approximately 3%.

Key Takeaway

In this blog post, using publicly available data, we confirm that high inflation leads to an inverse risk-return relationship, particularly after periods when equities were expensive. This mispricing of risky stocks, driven by investors using nominal discount rates and over-optimism, reduces expected returns. Low-risk stocks, however, are more resilient.

Currently, with the excess CAPE yield below 3% and inflation above 3%, expected returns are low. Historically, after such periods, the market return was close to zero, but factor strategies still delivered positive returns of about 3% after inflation. Therefore, while the immediate future may not be promising for the equity premium, it looks bright for factor premiums.