Last week we covered Goldman Sachs’ latest report on hedge funds, which are gleefully shorting again. It’s time we turned to the investment bank’s latest report on mutual funds, which contained this interesting nugget:

“Active share” is a percentage measure of the overlap of a fund’s holdings and its benchmark. The higher it is, the more the fund diverges from the positions and the weightings of its underlying index. A fund that has a 0 per cent active share is the perfect passive index fund, while one with a 100 per cent active share has zero in common with its benchmark.

The concept was first introduced by Martijn Cremers and Antti Petajisto in their 2006 paper How Active is Your Fund Manager? A New Measure That Predicts Performance, and was quickly embraced by many asset manager as a chest-thumping gauge of how bold and contrarian they are.

Understandably so, because Cremers and Petajisto seemingly proved what a lot of investors had long argued: fund managers more willing to diverge from their index are more likely to beat it, even after fees. Importantly, the paper found that a high active share actually seemed to predict outperformance.

Many asset managers therefore rushed out marketing to show how “active” they were, and the measure became a major weapon in the fight against passive investment funds, a cudgel to hammer lazy, expensive “closet indexers”, and a justification for charging higher fees for more active funds.

The widespread expectation was that in an era of rising active-share awareness, de facto index huggers would increasingly be found out, with their money flowing both into entirely passive funds and into genuinely active funds, which could accordingly charge more for their services. It was an enticing narrative for asset managers, and many expected active shares to edge higher over time as a result.

However, as Goldman Sachs notes, the active share of the 541 large US equity mutual funds it tracks — with $3.5tn of combined assets — has actually been trending down over the past decade. Interestingly, the phenomenon is particularly acute among “growth”-focused fund managers, while value-oriented ones have generally seen their active share drift higher.

However, the decline in active share has come as relative performance has started to improve this year — and, funnily enough, especially among the least-active growth managers.

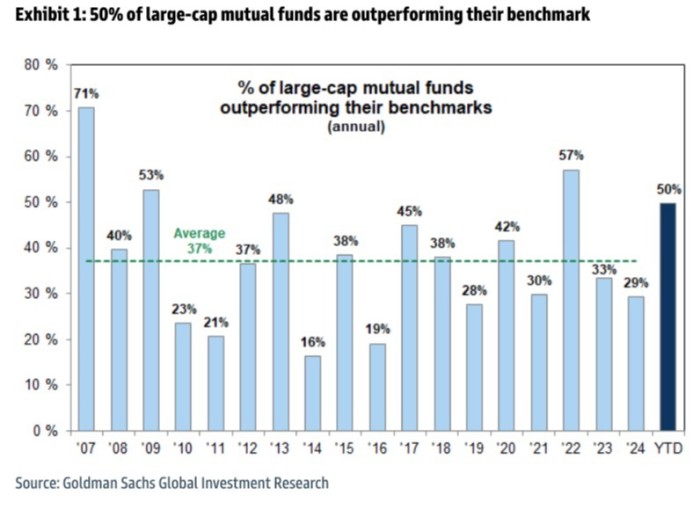

So far this year, 50 per cent of large-cap US equity mutual funds are outperforming their benchmarks, according to Goldman. That’s better than last year’s dismal 29 per cent beat rate, and the long-term average of 37 per cent. If it stays this way it will be one of the best years for active management in the past two decades.

Meanwhile, a whopping 67 per cent of large-cap growth funds are beating their indices, compared with 46 per cent of “core” funds and 38 per cent of value funds.

It’s tempting to treat correlation as causation here, and argue that active funds — increasingly worried about the consequences of single bad year of underperformance — are slowly morphing into semi-passive funds. As a result, you’d also expect average annual performance to coalesce around the average annual performance of the market (minus fees).

But as you might have spotted, the active share was also very low in 2024, when the average performance of active managers was miserable even by the standards of the past decade. Moreover, the Y-axis of the Goldman chart makes the decline in active share seem more pronounced; in reality it has just slipped from about 70 per cent to ca 65 per cent. Which is notable, but hardly dramatic.

Therefore, while the argument that some active funds are becoming increasingly cautious as a result of the growing consequences of even temporary underperformance is probably true, on the margins, we shouldn’t read too much into it.

Moreover, the link between active share and performance is actually a lot more tenuous than some people think. A 2015 paper by three AQR researchers — Andrea Frazzini, Jacques Friedman and Lukasz Pomorski — kicked the tyres of the original Cremers and Petajisto paper and found that while a fund’s active share correlates with returns, it doesn’t actually predict it. Moreover, “within individual benchmarks, it is as likely to correlate positively with performance as it is to correlate negatively,” they concluded.

Even this may now be overly optimistic. Morningstar revisited the topic again in 2021, and found that funds with higher active share had actually performed worse than the average since the publication of the first Cremers and Petajisto paper. This was both because they usually cost investors more, and because their performance had declined.

While highly active managers demonstrated some skill over the 18-year period through 2020, their superiority was mostly limited to the earlier half of that span. Their results from 2011 through 2020 give them little to brag about. Relative to lower-active-share peers, their before-fee results during that 10 year span were among the worst in seven of the nine categories and dead last in five. Only the high active-share quintile within the small-growth category showed excess gross returns — 0.5 percentage points annualized — while posting excess returns of negative 1.0 percentage points or worse in six categories. The lowest-active-share quintile performed best in four categories.

Why? Because the context matters.

Many big stock market indices have become more concentrated in recent years, and this explains a large chunk in the ebb and flow of active share measurements. For example, growth-oriented benchmarks like the Nasdaq have become increasingly top-heavy over the past decade, while, say, the Russell 1000 Value index has become less so. “That relationship explains both the current levels of median active share across categories and changes over time,” Morningstar’s Robby Greengold argued.

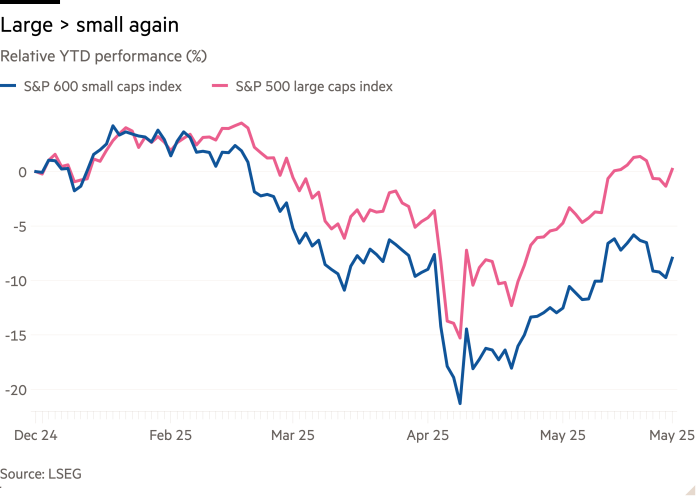

Moreover, because highly-active funds almost by definition tend to buy smaller stocks than what the index would dictate — whatever the benchmark they use — they usually to do well whenever smaller stocks do well. In other words, active share is in practice just the small-caps effect in a fancy costume.

As a result, highly-active funds tend to do better when small stocks do well (viz, the 1980-2003 period initially studied by Cremers and Petajisto), and tend to do worse when small-caps do badly (the 2011-2020 period examined by Morningstar). And right now, smaller stocks are once again blowing chunks relative to larger ones.

So what does this all mean?

Well, that the decline in active share is probably mostly an artefact of index concentration; that there is no single Holy Grail of investment metrics that you can use to predict performance; and that at the end of the year, most active managers will almost certainly have still underperformed their benchmarks. Plus ça change, plus c’est la même chose.