The following is based on “Redefining the Optimal Retirement Income Strategy,” from the Financial Analysts Journal.

Financial planning tools largely assume retirement spending is relatively predictable, that it increases annually with inflation regardless of an investment portfolio’s performance. In reality, retirees typically have some ability to adapt spending and adjust portfolio withdrawals to prolong the life of their portfolios, especially if those portfolios are on a declining trajectory.

Our latest research on perceptions around retirement spending flexibility provides evidence that households can adjust their spending and that adjustments are likely to be less cataclysmic than success rates and other common financial-planning-outcomes metrics imply. This suggests that spending flexibility needs to be better incorporated into the tools and outcomes metrics that financial advisers use to advise clients.

Flexible and Essential Expenses

Investors are often flexible on their financial goals. For example, a household’s retirement liability differs from a defined benefit (DB) plan’s liability. While DB plans have legally mandated, or “hard,” liabilities, retirees typically have significant control over their expenses, which could be perceived as “soft” to some extent. This is important when applying different institutional constructs, such as liability-driven investing (LDI), to households.

Most financial planning tools today still rely on the static modeling assumptions outlined in William P. Bengen’s original research. This results in the commonly cited “4% Rule,” where spending is assumed to change only due to inflation throughout retirement and does not vary based on portfolio performance or other factors. While the continued use of these static models may primarily be a function of their computational convenience, it could also be due to a lack of understanding around the nature of retirement liability, or the extent to which a retiree is actually comfortable adjusting spending as conditions dictate.

In a recent survey of 1,500 defined contribution (DC) retirement plan participants between the ages of 50 and 70, we explored investor perceptions of spending flexibility and found that respondents were much more capable of cutting back on different expenditures in retirement than the conventional models suggest. The sample was balanced by age and ethnicity to be representative of the target audience in the general population.

Ability to Cut Back on Various Spending Groups in Retirement

| Spending Group | 0% — Not Willing to Cut Back | Reduce by 1% to 24% | Reduce by 25% to 50% | Reduce by 50% or More |

| Food (At Home) | 29% | 42% | 21% | 7% |

| Food (Away from Home) | 12% | 41% | 25% | 20% |

| Housing | 31% | 29% | 22% | 12% |

| Vehicles/ Transportation |

13% | 46% | 26% | 13% |

| Vacations/ Entertainment |

14% | 36% | 25% | 20% |

| Utilities | 31% | 45% | 16% | 8% |

| Health Care | 43% | 30% | 17% | 8% |

| Clothing | 6% | 44% | 25% | 22% |

| Insurance | 32% | 40% | 19% | 8% |

| Charity | 18% | 31% | 12% | 19% |

According to traditional static spending models, 100% of retirees would be unwilling to cut back on any of the listed expenditures. In reality, though, respondents demonstrate a relatively significant ability to adjust spending, with notable variations across both expenditure type and households. For example, while 43% of respondents wouldn’t be willing to cut back on health care at all, only 6% would say the same about clothing. In contrast, certain households are more willing to cut back on health care expenditures than vacations.

A spending cut’s potential cost may not be as severe as traditional models imply. For example, models generally treat the entire retirement spending goal as essential: Even small shortfalls are considered “failures” when the probability of success is the outcomes metric. But when we asked respondents how a 20% drop in spending would affect their lifestyle, most said they could tolerate it without having to make severe adjustments.

Impact of a 20% Spending Drop on Retirement Lifestyle

| Little or No Effect | 9% |

| Few Changes, Nothing Dramatic | 31% |

| Some Changes, But Can Be Accommodated | 45% |

| Substantial Changes and Considerable Sacrifices | 13% |

| Devastating, Would Fundamentally Change Lifestyle | 2% |

For example, only 15% said a 20% spending drop would create “substantial changes” or be “devastating” to their retirement lifestyle, while 40% said it would have “little or no effect” or necessitate “few changes.” Retirees appear to be far more sanguine on a potential reduction in spending than traditional models would suggest.

The clear ability to cut spending as demonstrated in the first chart, and the relatively small implied potential impact on retiree satisfaction, or utility, in the second, at least for a relatively small change in spending, has important implications when projecting retirement income goals. While understanding each retiree’s spending goal at the more granular expenditure level is important, so too is having a sense of what amount of spending is “essential” (i.e., “needs”) and “flexible (i.e., “wants”) when mapping out assets to fund retirement liabilities. The following chart provides some context on what percentage of the total retirement income goal constitutes “needs.”

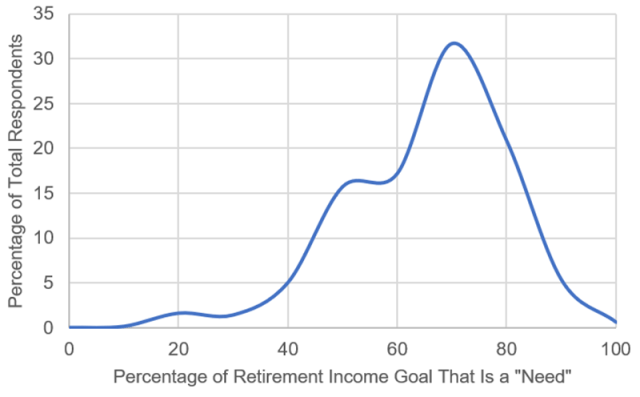

Distribution of Responses: The Composition of a Retirement Goal That Is a “Need” (Essential)

While the average respondent says that approximately 65% of retiree spending is essential, there is notable variation: The standard deviation is 15%.

Spending flexibility is critical when considering the investment portfolio’s role in funding retirement spending. Virtually all Americans receive some form of private or public pension benefit that provides a minimum level of guaranteed lifetime income and can fund essential expenses. In contrast, the portfolio could be used to fund more flexible expenses, which are a very different liability than is implied by static spending models that suggest the entire liability is essential.

Conclusions

Overall, our research demonstrates that retirement spending is far more flexible than implied by most financial planning tools. Retirees have both the ability and the willingness to adjust spending over time. That’s why incorporating spending flexibility can have significant implications on a variety of retirement-related decisions, such as required savings level (generally lower) and asset allocations (generally more aggressive portfolios may be acceptable, and certain asset classes become more attractive).

For more from David Blanchett, PhD, CFA, CPA, don’t miss “Redefining the Optimal Retirement Income Strategy,” from the Financial Analysts Journal.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / Paul Sutherland

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

")