Factors are the primary market drivers of asset-class returns. In the equity realm, only a limited set of rewarded factors are backed by academic consensus: Value, Size, Momentum, Low Volatility, High Profitability, and Low Investment. These factors compensate investors for the additional risk exposure they create in bad times. Hence, factor strategies are appealing to investors because they provide exposure to rewarded risk factors in addition to market risk and can be a source of superior risk-adjusted performance over the long term compared with cap-weighted benchmarks.

The year 2022 was a memorable one for investors, but for not altogether positive reasons. One bright spot, however, was the relative outperformance of equity risk factors versus other popular equity investing styles. While the financial media has attributed recent strong factor performance almost entirely to the Value factor, the resurgence of factor performance was in fact much broader.

Factor Performance’s Comeback Was Broad Based

Here “factor performance” refers to the performance of long/short factor portfolios that go long a subset of stocks with the strongest positive exposure to a given factor and short a subset of stocks with the strongest negative exposure to the same factor. Indeed, in the United States, almost all factors had positive performance in 2022, with an average return of 6.9%, which is in line with their long-term average, as illustrated in the chart below. Momentum, Low Investment, and Value factors beat their long-term average, though not their best 5% annual rolling returns. The Low Volatility and Size factors also had positive performance albeit below their long-term average. High Profitability was an outlier, posting the only negative performance. Indeed, the factor fared so poorly, it eclipsed its worst 5% rolling return between 31 December 1974 and 31 December 2021.

US Factor Performance in 2022

| US Factors | Size | Value | Mom | Low Vol | High Pro | Low Inv | 6-F EW |

| 2022 | 3.5% | 8.4% | 19.9% | 4.3% | -10.1% | 15.4% | 6.9% |

| Avg. Rolling Annual Return |

8.8% | -1.7% | 3.9% | 8.5% | 3.8% | 4.1% | 4.1% |

| Worst 5% Rolling Return |

-22.0% | -20.5% | -20.9% | -17.4% | -9.1% | -9.2% | -3.9% |

| Best 5% Rolling Return |

53.8% | 14.4% | 27.9% | 36.9% | 22.5% | 21.3% | 18.7% |

The results in the chart above contradict two popular media narratives: that the factor performance story is solely a Value story and that any highly profitable company will outperform in a rising rate environment.

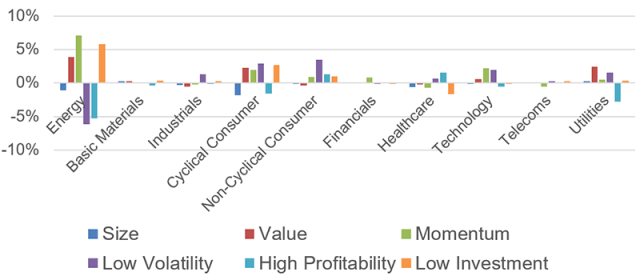

The Factor Story Has Been a Sector Story

Which sectors drove factor performance in 2022? The energy sector played an outsized role. It outperformed its broad cap-weighted counterpart by 84.5% and, as the exhibit below illustrates, helped drive Value, Momentum, and Low Investment factor performance and negatively impacted Low Volatility and High Profitability.

Sector Performance Attribution: US Factors, 2022

For international equities and global equities, the story is largely consistent with the US market.

Factor Performance through a Macro Lens

While macro factors are not the primary drivers of equity performance, they can have significant influence on factor behavior in certain environments. In examining how the macro environment influences factor performance, we use a macro framework developed by Noël Amenc, Mikheil Esakia, Felix Goltz, and Ben Luyten. Our four macro variables, shown in the chart below, are short rates (three-month Treasury bills); term spread (10-year minus 1-year Treasuries); default spread (Baa minus Aaa Corporate Bonds); and breakeven inflation (10-year break-even inflation). For each macro variable, we build a long/short macro portfolio composed of stocks with the strongest and weakest sensitivity to macro innovations (surprises). We go long stocks with the highest sensitivity to weekly macro innovations and short stocks with the lowest sensitivity to weekly macro innovations.

In 2022, macro factors explained much of the variability of some US equity factors. For instance, term spread, credit spread, and breakeven inflation factors, respectively, explained 27%, 33.7%, and 45.3% of the Value factor’s variability over the period. Breakeven inflation was one of the strongest macro factors since it explained a large part of the return variability of Value, High Profitability, and Momentum. No macro factor had a real impact on the variability of the Momentum factor.

Percentage of 2022 US Equity Factor Performance Explained by Macro Factors

| US 2022 R-Squared |

Size | Value | Momentum | Low Volatility |

High Profitability |

Low Investment |

| Short Rate | 6.1% | 0.4% | 0.6% | 46.7% | 8.0% | 1.0% |

| Term Spread | 8.6% | 27.0% | 1.2% | 36.3% | 36.5% | 11.7% |

| Credit Spread | 11.4% | 33.7% | 5.3% | 20.5% | 47.1% | 22.4% |

| Breakeven Inflation |

12.5% | 45.3% | 7.1% | 19.6% | 67.0% | 29.7% |

The results above are a contrast to the longer-term impact of macro factors on equity factors, depicted in the following chart. While macro factors do not have the most significant impact over the longer term, given the transition to a more normalized interest rate environment, they do exert a more pronounced effect on 2022 factor performance. This is consistent with academic findings. Indeed, factor risk premia short-term variations are linked to the business cycle or macroeconomic conditions.

Percentage of US Equity Factor Longer-Term Performance Explained by Macro Factors

| US Long-Term R-Squared |

Size | Value | Momentum | Low Volatility |

High Profitability |

Low Investment |

| Short Rate | 0.9% | 5.9% | 6.0% | 29.4% | 1.2% | 14.5% |

| Term Spread | 1.9% | 1.2% | 0.0% | 14.9% | 3.7% | 0.8% |

| Credit Spread | 4.7% | 0.3% | 0.0% | 21.7% | 0.0% | 7.1% |

| Expected Inflation | 0.4% | 3.2% | 0.2% | 4.9% | 10.3% | 0.8% |

How did macro factors affect equity factors? The chart below shows Value and Low Investment had positive sensitivity and High Profitability and Low Volatility negative sensitivity to breakeven inflation. Similarly, Value and Low Investment had negative sensitivity and Low Volatility and High Profitability positive sensitivity to the credit spread factor.

2022 US Equity Factor Sensitivities to Macro Factors

| US 2022 Betas |

Size | Value | Momentum | Low Volatility |

High Profitability |

Low Investment |

| Short Rate | 0.22 | 0.05 | -0.04 | -1.11 | -0.25 | -0.08 |

| Term Spread | 0.16 | 0.33 | 0.07 | -0.62 | -0.35 | 0.23 |

| Credit Spread | -0.33 | -0.65 | -0.34 | 0.83 | 0.71 | -0.57 |

| Breakeven Inflation |

0.25 | 0.54 | 0.28 | -0.58 | -0.60 | 0.46 |

What’s Next for Factors?

While predicting how factors will behave in 2023 and beyond is impossible, thus far it seems like the macroeconomy, especially monetary policy, will still be at the forefront of investors’ minds. How that will influence sectors and factors is an even more difficult question, and investing based on a specific macroeconomic outcome may not be the best course of action for most investors. Rather, investing across the set of rewarded factors may be more advisable. As empirical evidence shows, the factors’ average historical premia will likely be able to weather all kinds of extreme market conditions and macro developments. The long-term reward of risk factors will not fade because they are compensation for additional risks investors are taking. Hence, multi-factor strategies with well-balanced exposures to the six rewarded factors should continue to benefit from their long-term reward in the future.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images / baona

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.