Scope 3 disclosures are complex, and Category 15 (Investments) is an obscure segment intended to cover emissions that arise from one company having a stake in another (i.e., financial transactions)1. For most companies, this represents a proverbial footnote in their overall emissions profile. Indeed, given Category 15’s unique set of conceptual and data challenges, it is not a coincidence that it sits at the tail end of the Scope 3 catalogue.

For financial institutions, however, financial transactions are the business, making Category 15 emissions a critical component of their overall emissions disclosures.

Compared to other industries, financial institutions typically produce low Scope 1 and 2 emissions, which mostly come from offices and electricity use. Financial institutions produce limited emissions from most Scope 3 categories, and these emissions are linked mostly to their purchased goods and services and business travel.

In contrast, their Category 15 emissions are exceptionally large. On average, more than 99% of a financial institution’s overall emissions footprint comes from Category 15 emissions.2

Financed and Facilitated Emissions

Financial institutions’ Category 15 emissions include financed emissions and facilitated emissions. Financed emissions are on-balance-sheet emissions from direct lending and investment activities. These include the emissions from a company that a bank provides a loan to or in which an asset manager holds shares. Facilitated emissions are off-balance-sheet emissions from enabling capital market services and transactions. An example is the emissions from a company that an investment bank helps to issue debt or equity securities or for which it facilitates a loan through syndication.

Financed and facilitated emissions are key to understanding the climate risk exposure of financial institutions. This could be substantial, for example, for a bank with a large lending book focused on airlines or an insurance firm specialized in oil and gas operations. So, it is not surprising that various stakeholders have been advocating for more disclosures. These include the Partnership for Carbon Accounting Financials (PCAF), the Principles for Responsible Investing (PRI), the Glasgow Financial Alliance for Net Zero (GFANZ), the Science Based Targets Initiative (SBTi), CDP, and the Transition Pathway Initiative (TPI).

As Scope 3 disclosures are becoming mandatory in several jurisdictions, this takes on even greater urgency for the finance industry. The European Union’s Corporate Sustainability Reporting Directive, for example, requires all large companies listed on its regulated markets to report their Scope 3 emissions, and similar requirements are emerging in other jurisdictions around the world. While disclosure regulations usually don’t prescribe which Scope 3 emissions categories should be included in disclosures, they typically ask for material categories to be covered, making it difficult for financial institutions to argue against disclosing their financed and facilitated emissions.

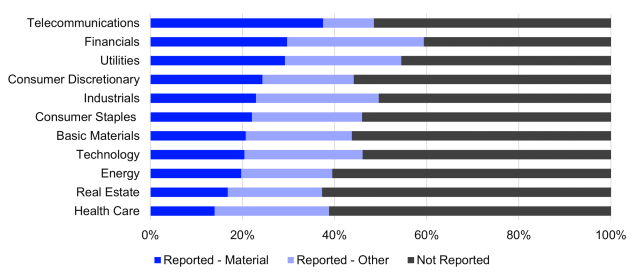

This poses a considerable challenge. Exhibit 1 shows that financial institutions’ Scope 3 reporting rates are among the highest across all industries. Only a third disclose their financed emissions, and they often only cover parts of their portfolios.3 To date, only a handful have attempted to disclose their facilitated emissions. A recent report from the TPI examining the climate disclosures of 26 global banks shows that none have fully disclosed their financed and facilitated emissions.4

Three Key Challenges

Financial institutions need to overcome three key challenges in disclosing their financed and facilitated emissions to improve corporate reporting rates.

First, in contrast to other Scope 3 categories, the rulebook for reporting on financed emissions and facilitated emissions is in many ways still nascent and incomplete. Accounting rules for financed emissions were only finalized by PCAF and endorsed by the Greenhouse Gas (GHG) Protocol — the global standard setter for GHG accounting — in 2020.5 These codify the accounting rules for banks, asset managers, asset owners and insurance firms. Rules for facilitated emissions followed in 20236, covering large investment banks and brokerage services. Those for reinsurance portfolios are currently pending the approval of the GHG Protocol7, while rules for many other types of financial institution (not least exchanges and data providers like us) currently don’t exist.

Exhibit 1.

Source: LSEG, CDP. Companies reporting material and other Scope 3 vs non-reporting companies, in 2022 FTSE All-World Index, by Industry

In practice, financial institutions often lack robust emissions data for large parts of their diverse client base. Such data is often available for large, listed companies, but rarely available for privately held companies or SMEs that commonly make up large shares of financial institutions’ client books. This can lead to huge data gaps in the emissions data inventory of financial institutions.

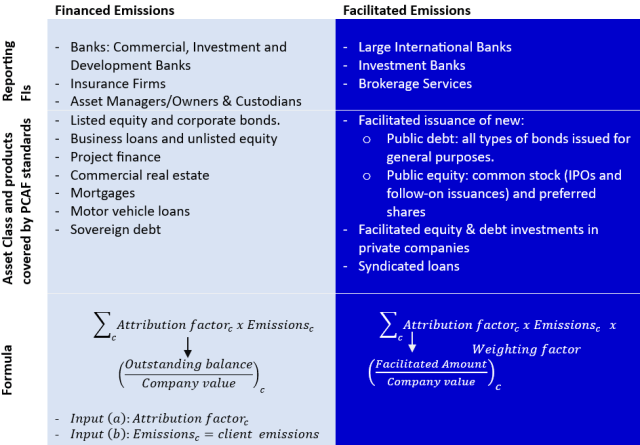

Exhibit 2. Features of PCAF’s Financed and Facilitated emissions standards5,6

Third, there are complexities around attribution factors. For financed emissions, this is the ratio of investments and/or outstanding loan balance to the client’s company value. However, market fluctuations of share prices complicate this picture and can result in swings in financed emissions that are not linked to the actual emissions profile of client companies.8

The same problem persists for facilitated emissions, but worse. Determining appropriate attribution factors is often conceptually difficult due to the myriad different ways that financial institutions facilitate financial transactions, from issuing securities to underwriting syndicated loans. As the Chief Sustainability Officer of HSBC recently explained,9 “This stuff sometimes is hours or days or weeks on our books. In the same way that the corporate lawyer is involved in that transaction, or one other big four accounting firms is involved…they are facilitating the transaction. This is not actually our financing.”

Next Steps?

Given these complexities and the significant reporting burden, financed and facilitated emissions are likely to remain a headache for reporting companies, investors, and regulators alike for some time to come.

Meanwhile, proxy data and estimates are likely to play an important role in plugging disclosure gaps. One tangible way forward could be to encourage financial institutions to provide better disclosures on the sectoral and regional breakdown of their client books. This is readily available, if rarely disclosed, data. This could allow investors and regulators to gain a better, if imperfect, understanding of the transition risk profile of financial institutions while reporting systems for financed and facilitated emissions continue to mature.

Resources

FTSE Russell’s Scope for Improvement report addresses 10 key questions about Scope 3 emissions and proposes solutions to enhance data quality.

In its Climate Data in the Investment Process report, CFA Institute Research and Policy Center discusses how regulations to enhance transparency are evolving and suggests how investors can make effective use of the data available to them.

Footnotes