It’s often claimed that small-cap stocks are more interest-rate sensitive than their large-cap counterparts because of their reliance on outside financing. This seems plausible. But what do the data say?

In this blog post, I explore the relationship between small- and large-cap stocks and interest-rate changes using the Stocks, Bonds, Bills and Inflation® (SBBI®) monthly dataset — which is available to CFA Institute members — and the Robert Shiller long-bond rate dataset. I use graphs and correlations (and a little regression).

My main findings are:

- Small-stock monthly returns are no more sensitive to rate changes than large-stock returns.

- Small stocks fare no worse on average than large stocks during periods of Federal Reserve (Fed) interest-rate tightenings, where tightening periods are as defined by Alan Blinder in a recent paper.

- The relationship between stocks and rates isn’t stable. There are periods when equities are highly rate sensitive, and periods when they aren’t.

- The Federal Reserve Bank of Chicago’s (Chicago Fed’s) National Financial Conditions Index (NFCI) — a proxy for ease of overall access to capital — has about the same relationship with small-stock returns as with large.

R Code for calculations performed and charts rendered can be found in the online supplement to this post.

Stocks and Rates: The Big Picture

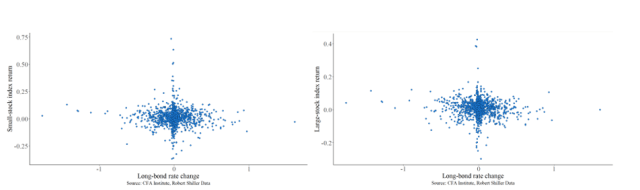

I start with the full period for the SBBI® dataset: January 1926 to April 2024. The left panel in Chart 1 shows the correlation between small-stock monthly returns and the long-government bond interest rate (hereafter, the “long rate” or just “rate”) from the inception of the SBBI® dataset in 1926 to April 2024, which is the last available month of SBBI® returns. The right panel in Chart 1 shows the correlation between large-stock monthly returns and the long rate during the same period.

The correlation between large stocks and rate changes is modestly negative (-0.1) and significant at the 95% level. The correlation between small stocks and rate changes is not significant. These results are robust to lagging the rate change variable by one period and to restricting rate changes to positive values. That is, accounting for possible delayed effects and limiting rate changes to the potentially adverse doesn’t change the results.

Chart 1. Monthly small- (left) and large-stock (right) returns versus long-rate changes, 1926 to April 2024.

These correlations are suggestive, but obviously not conclusive. The long timeframe — nearly a century — could mask important shorter-term relationships.

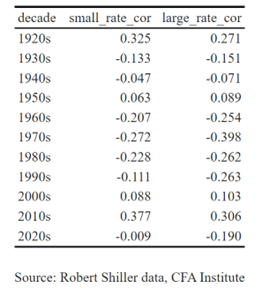

Table 1 therefore shows the same statistic but grouped, somewhat arbitrarily, by decade.

Table 1. Large- and small-cap stock monthly return correlations with all long rate changes.

When viewed this way, the data suggest that there could be meaningfully long periods when correlations differ from zero. I omit confidence intervals here, but they don’t include zero when correlations are relatively large in an absolute sense. Correlations are usually of the expected sign (negative).

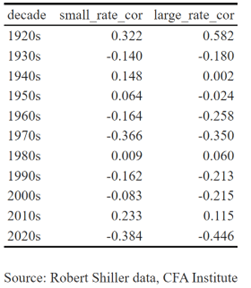

There doesn’t seem to be much difference in the way that small and large stocks respond to long-rate changes, with the possible exception of the last few years (the 2020s). These findings are robust to lagging the rate-change variable by one period. Restricting rate changes to positive observations changes both the sign of correlations and (significantly) their magnitude in some periods, as shown in Table 2. Nothing about Table 2’s results, however, suggests a difference in the reaction of small and large stocks to a rise in rates.

Table 2. Large- and small-cap stock monthly return correlations with positive long-rate changes.

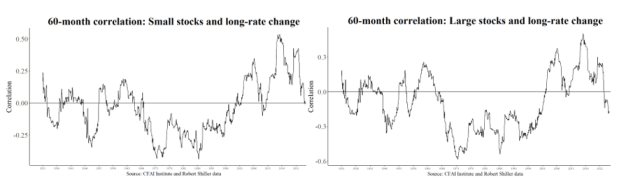

But, as noted, decades are arbitrary periods. Chart 2 therefore shows the rolling 60-month correlation between the small-, large-, and long-rate change series for the length of the SBBI® dataset.

Chart 2. Rolling 60-month correlations between small (left) and large (right) stocks and long-rate changes.

Two features are noteworthy. One, the charts are nearly indistinguishable visually, vertical-axis values aside. Small and large stocks appear to exhibit similar behavior in response to rate changes. It’s hard to avoid the inference that small-cap stocks don’t respond differently to long-rate changes than large-cap stocks. And two, the stock-rate relationship varies, and can have the “wrong” sign for long periods.

Removing Market Effects

Could the observed similar response of large and small stocks to long-rate changes be due to the influence of “the market” (large-stock returns) on small stocks? It seems plausible that broad market effects could mask an adverse reaction of small stocks to rising borrowing costs. Removing them might give us a better sense of the effect of long-rate changes on small-stock returns.

I do this by first regressing small-stock monthly returns on large-stock monthly returns (a proxy for “the market”). I then calculate partial correlation using the residuals from this regression, which reflect the non-market part of small-stock returns and long-rate changes.[1]

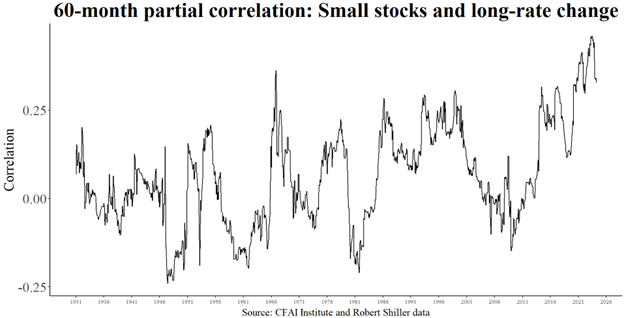

Overall (1926 – April 2024), the partial correlation is again not different from zero. However, as shown in Chart 3, the rolling, 60-month partial correlation has been mostly (though not always) positive — the opposite of the expected sign — and sometimes large, particularly lately. Controlling for “market beta” therefore does seem to impact the relationship between small stocks and long rates. These results probably aren’t practically meaningful or useful, however.

Chart 3. Rolling 60-month partial correlations between small stocks and rate changes.

Monetary Policy and Returns

Small-cap stocks could be more sensitive to shorter-term rates to which their borrowing costs are more closely linked.

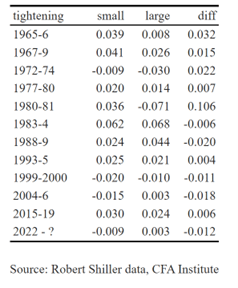

Table 3 therefore shows the average annualized performance (in decimals, so, e.g., 0.03 = 3%) of small and large stocks during the 12 Fed tightening episodes identified by Alan Blinder (listed in column 1) in his paper on “soft landings.”

Table 3. Large- and small-stock performance during Blinder’s monetary tightenings.

Before the early 1980s, a researcher might have concluded that small stocks performed better than large stocks when the Fed was hiking. The fourth column (“diff”), which shows the difference between small and large stock returns, was positive in all tightenings up to that time.

Since then, small stocks have underperformed during tightenings more often than they’ve outperformed. But the difference seems modest.

Financial Conditions

Perhaps Fed-induced short-term rate increases and long-rate rises don’t adequately proxy for availability of credit.

Helpfully, the Chicago Fed maintains the NFCI, which summarizes financial conditions using a weighted average of more than 100 indicators of risk, credit, and leverage. The smaller (more negative) the NFCI’s value, the looser (more accommodative) are financial conditions.

The conventional wisdom that small stocks are disadvantaged relative to large stocks in less-hospitable financial conditions suggests a negative correlation between the NFCI and small-stock returns. And deteriorating financial conditions, as reflected by positive NFCI values, should be more negatively related to small-cap returns than to large-cap returns.

To test this, I first remove possible NFCI time trends by differencing (subtracting from each value the previous value) the series, which shouldn’t change the expected correlation sign (negative). Then, I repeat the calculations above. I find no difference in the response of small and large stocks to changes in financial conditions as shown in the online supplement to this blog. In neither case does the change in the NFCI or its lagged value appear related to returns.

Avoid Broad Statements About Small Stocks and Rates

Using CFAI SBBI® and Robert Shiller data on long-government bond rates, I don’t find evidence to support the claim that small and large stocks respond to rate changes differently. Additionally, small and large stocks don’t react differently to the short-term rate rises that occur during Fed tightenings or to the changes in capital-market activity as measured by a broad financial conditions index.

As Table 1 shows, stock returns and rate changes were almost always inversely related until the decade following the Great Recession, and to roughly the same degree. Table 3 points to the same conclusion for episodes of Fed tightening.

The former result is consistent with theory. The latter is contrary to the conventional wisdom that small stocks (as proxied by the SBBI® small-cap index) are uniquely vulnerable to rising rates.

You May Also Like

Monetary Policy and Financial Conditions: Meaningful Relationship?

The author is a Registered Investment Advisor representative of Armstrong Advisory Group. The information contained herein represents Fandetti’s independent view or research and does not represent solicitation, advertising, or research from Armstrong Advisory Group. It has been obtained from or is based upon sources believed to be reliable, but its accuracy and completeness are not guaranteed. This is not intended to be an offer to buy, sell, or hold any securities.

[1] This could of course also be estimated using the multiple regression of small-stock returns on interest rates, controlling for large-stock returns.

Suffers a Larger Drop Than the General Market: Key Insights")