Updated on July 8th, 2025 by Felix Martinez

H.B. Fuller (FUL) has increased its dividend for 56 consecutive years. That puts the company among the elite Dividend Kings, a small group of stocks that have increased their payouts for at least 50 consecutive years.

You can see the complete list of all 55 Dividend Kings here.

We have compiled a comprehensive list of all Dividend Kings, along with key financial metrics such as price-to-earnings ratios and dividend yields. You can access the spreadsheet by clicking on the link below:

H.B. Fuller has remained a relatively small company, trading at a market capitalization of just $3.3 billion. However, a small market cap is not a negative feature when investing; quite the contrary.

Despite its small size, H.B. Fuller has promising growth prospects thanks to the growth potential of the niche market in which it operates. The stock offers a 1.6% dividend yield, which is higher than the yield of the S&P 500.

However, there is ample room for future dividend raises, thanks to the company’s low payout ratio and strong growth prospects.

Business Overview

H.B. Fuller is a global market leader in adhesives, sealants, and other specialty chemical products. It has 69 manufacturing facilities and 38 technology centers and sells its products in 125 countries.

Adhesives are a desirable niche market. Adhesives are critical materials in numerous applications, but they comprise just a small expense for H.B. Fuller’s customers. Adhesives make up less than 1% of the cost of goods for most customers.

In addition, each adhesive has unique chemistry, with most product formulations including 3-10 chemicals. It is also uneconomical for customers to switch to another supplier.

Overall, H.B. Fuller’s customers must use its essential products without paying much attention to their cost, which is minor compared to other costs.

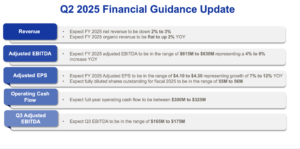

H.B. Fuller reported Q2 2025 net income of $41.8 million ($0.76 per diluted share), down 18.4% from $51.3 million ($0.91 per diluted share) in Q2 2024. Adjusted EPS rose 5% to $1.18, driven by higher adjusted net income and fewer shares. Net revenue fell 2.1% to $898.1 million, but organic revenue grew 0.4%, with pricing up 0.7%, offset by lower volume, a 1.2% currency headwind, and a 1.3% impact from divestitures. Adjusted EBITDA increased 5% to $166 million, with a margin of 18.4% (up 130 basis points), reflecting cost savings and pricing actions.

Gross profit was $286.4 million, with an adjusted gross margin of 32.2% (up 110 basis points). Adjusted SG&A expenses were flat at $176 million. Operating cash flow rose 35.4% to $111 million. Net debt was $2.016 billion, down $59 million, with a net debt-to-adjusted EBITDA ratio of 3.4X. The company repurchased 1 million shares year-to-date.

H.B. Fuller raised its 2025 guidance, expecting net revenue down 2–3%, organic revenue flat to up 2%, adjusted EBITDA of $615–$630 million (4–6% growth), and adjusted EPS of $4.10–$4.30 (7–12% growth). CEO Celeste Mastin emphasized the importance of strong execution and portfolio optimization, positioning the company to outperform in a challenging global market.

Source: Investor Presentation

Growth Prospects

Thanks to the high fragmentation of this market, there is a significant growth potential for H.B. Fuller, which has consistently been the second-largest player in the market behind Henkel.

Moreover, H.B. Fuller enjoys economies of scale that its smaller competitors cannot match, while the latter also lack the global reach to compete directly with H.B. Fuller. As a result, H.B. Fuller is likely to keep growing by gaining market share from its small competitors over time.

Source: Investor Presentation

H.B. Fuller is also likely to keep growing via significant acquisitions. In 2017, it acquired Royal Adhesives & Sealants for $1.6 billion. As the value of that acquisition is about 38% of the current market capitalization of H.B. Fuller, it is evident that the merger, the largest in the company’s history, was critical.

The acquisition enhanced H.B. Fuller’s product range to include more specialized adhesives and boosted its annual sales by approximately $735 million (32%).

Since the acquisition, H.B. Fuller has been reducing its debt load at a fast pace. When that process is complete, H.B. Fuller will shift its focus again to potential takeover targets. The company also acquired Adecol in late 2017 in order to enhance its growth potential in Brazil.

H.B. Fuller has grown its earnings per share at an average annual rate of 7.5% over the past seven years and 10.6% over the past five years. The company has emerged stronger from the pandemic and has provided guidance for an improvement in its adjusted EBITDA.

Overall, we expect H.B. Fuller to grow its earnings per share at a 6.0% average annual rate over the next five years, roughly in line with its historical growth pace.

Competitive Advantages & Recession Performance

H.B. Fuller’s customers manufacture a wide range of products. Consequently, the performance of H.B. Fuller greatly depends on the prevailing economic conditions, and thus, the company is vulnerable to recessions. During the Great Recession, its earnings per share plummeted 79%, from $1.68 in 2007 to $0.36 in 2008, and the stock lost two-thirds of its market capitalization in under six months.

Still, the wide range of applications of its adhesives provides some diversification. For example, during the pandemic, strong growth in demand for health and hygiene products largely offset the decrease in demand for adhesives in other categories. As a result, earnings per share dipped only 3% in 2020, an admirable performance for an industrial company.

Moreover, H.B. Fuller is the #1 or #2 player in most of its markets, and thus, it can endure a downturn more readily than its small competitors, thanks to its economies of scale. It is also worth noting that its top 10 customers account for a relatively small portion of its revenue, and thus, the company has limited risk from any specific customer.

Finally, it is impressive that an industrial manufacturer closely tied to the underlying economic growth has raised its dividend for 56 consecutive years.

This is a testament to this niche market’s strong growth and the company’s excellent business execution. H.B. Fuller has achieved this exceptional dividend growth record partly thanks to its low payout ratio.

The company has consistently targeted a payout ratio of around 25% and has therefore been able to maintain its dividend growth even in years when its earnings have temporarily declined. Due to the low payout ratio, the dividend is safe, but the resultant 1.6% dividend yield is lackluster.

Valuation & Expected Returns

H.B. Fuller is currently trading at 15.2 times its expected earnings per share of $4.15 this year. While the historical earnings multiple of the stock is 18.5, we believe a fair price-to-earnings ratio is 15.0, considering the stock’s cyclical nature. If the stock reaches our fair valuation level over the next five years, it will suffer a 0.1% annualized headwind in its returns.

Given 6% expected earnings-per-share growth, the 1.6% dividend, and a -0.1% impact of a contracting price-to-earnings multiple, we expect H.B. Fuller to offer a 7.5% average annual total return over the next five years. This rate of return renders the stock a “Hold” at its current stock price of $62.

Final Thoughts

H.B. Fuller is highly vulnerable to recessions, but it proved markedly resilient during the pandemic, thanks to a substantial increase in the demand for adhesives used in health and hygiene products.

Moreover, thanks to the reliable long-term growth of its niche market and its high fragmentation, H.B. Fuller is likely to grow its earnings per share at a mid-single-digit rate in the upcoming years.

However, the company also appears to be somewhat overvalued, while the 1.6% dividend yield is relatively low. As a result, we advise investors to wait for a meaningful correction in H.B. Fuller’s stock price before purchasing it.

Additional Reading

The following articles contain stocks with very long dividend or corporate histories, ripe for selection for dividend growth investors:

Thanks for reading this article. Please send any feedback, corrections, or questions to support@suredividend.com.