I meant to write this post 2 weeks after the April 2 tariff announcement but life got in the way. So I would only get down to writing about it now.

Readers who are in retirement or in retirement might be wondering what does the recent increased risks due to many things mean to your retirement income plan.

I want to explore this topic briefly and perhaps bring in my Daedalus Income portfolio into the discussion.

I got a hunch many income planners suddenly felt unnerved mostly because what may seem like a foolproof or well thought out strategy, suddenly has question marks.

If you dig deeper, there seem to be shifts in the world that makes your plan feels more uncertain.

I can list a few:

- A stable USD now does not seem so stable anymore. This is especially worrying if you are 100% invested in an S&P 500 or a US denominated fund/ETF.

- Capital that was flowing into the US fixed income and equity market reversing its course.

- Not sure if the capital is coming back. And if part of the reason the equity market has done so well is due to this reason, then what about markets in the future.

- A president or a government that wishes to try and fix a huge trade deficit.

- Rising bond yields tend to be positive for equities, but not when the reason is that people don’t want to buy your debts anymore.

- Rising geo-political tensions and a cold war with China.

- What is the result of capital controls of USD outside and in US and how does that affect your investments?

- An imminent recession.

- A permanently higher interest rate environment.

I should have missed out on a few more things but the general feel might make you ponder more about the plan that you have.

Many plan with the idea that when you retire if I can hit 7% p.a. return over the time I need the income, I spend 4% p.a. and there should be 3% for the income to grow with inflation.

My friend told me in a conversation a year ago, due to these reasons, he doesn’t think his portfolio will hit that 7% p.a. return (or the number in his mind), and what are my thoughts about his plan.

The questions to me, or what I heard in the webinars with clients and prospects at work boil down to a few evergreen concepts and I want to spend a few short paragraphs to explore them.

1. Your Income Plan Live and Die by Returns if You Think Returns is the Most Critical Factor

If you have in mind that the US markets made 10-14% p.a. for the past 10 years and that return is critical for the success of your income plan, then you ought to be concern when you realize that the environment in the next 30 years might be different than in the past 10 years.

Many income planners happen to be investors and when they hit this problem, they think the issue might be that they have to shift their portfolio strategically (long term holdings) to something else.

For example, cannot just buy US stocks anymore must buy European stocks. Now unattractive Singapore securities might look more appealing because of the returns uncertainty outside of Singapore. Need to add gold.

The uncertainties that I listed above will still be around, and that uncertainties will be the same uncertainties that you invest in, be it European stocks, gold, energy, Singapore stocks, fixed income long maturity or short maturity.

A simple minded target or plan return makes your brain focus on an unrealistic number and make you feel that your plan will live and die by that investment return.

Income planners may have to accept the reality that they failed to see or keep denying all these while:

- The returns that they will get in the future is in a range. There is a way to figure out the range with the help of history if it is long enough but the returns will be in a range.

- There were uncertainties in the past when you did your initial plan but you may choose not to consider it.

- For the next 30 years where you need the income, the geopolitical landscape, markets, interest rates, inflation and currency is going to keep shifting.

Many don’t seem to be able to accept the reality they cannot control the returns and therefore they cannot control their income plans. If they fail to control returns, it also means their income is going to be volatile.

The hardest thing for them to accept might be returns is not the most critical factor when doing income planning.

2. An Income Plan is one Where You Surround Your Investments with a Sensible, Conservative Spending Strategy.

I think in income planners’ minds there is too much link between product income distribution and their spending.

They let that dictate their spending.

Either because they don’t trust themselves, think the fund manager of that income fund has their best interest, know their personal needs or a mixture. If it is not a product, they hunt for a suitable investment strategy for retirement income.

If you start separating the two (your income plan and your investments), you might realize that you don’t have to be dictate so much by what you buy.

Let me give you one example, suppose you have a $2 mil investment property that currently gives you a net rental income of $60,000 a year. If your income needs is $50,000 a year, do you consider yourself to be able to quit work (leaving other considerations aside) because of this?

A less experience property owner would think that their $60k income will remain stable and continue to go up over time. But the owner who owns the property for 20 years would remind themselves of the time that the same property rents only for 40% less and the net rental income ends up at $30,000 a year.

There is no currency risk, interest rate risk here, but we can see the direct income distribution is just more uncertain.

A sensible and conservative spending strategy starts by considering these reality. Such as returns are just going to be uncertain.

And most will build things into their income plan, but they don’t call this their income plan:

- Have enough cash buffers for 3 – 5 years of spending.

- Make conservative estimation of returns (which they actually mean how much they will take out from their consolidated portfolio)

- Have some weird decision-tree logics of “in the event of X, I will take from this portfolio A, and in the event of Y, I will take from Portfolio B instead.”

What they are trying to do is to create a spending system more independent of their investments.

The more you do this, the more you are telling yourself that returns are uncertain and I want to take back the control.

If you are coming up with a spending plan, here are some considerations if these uncertainties made you feel that your plan is less complete:

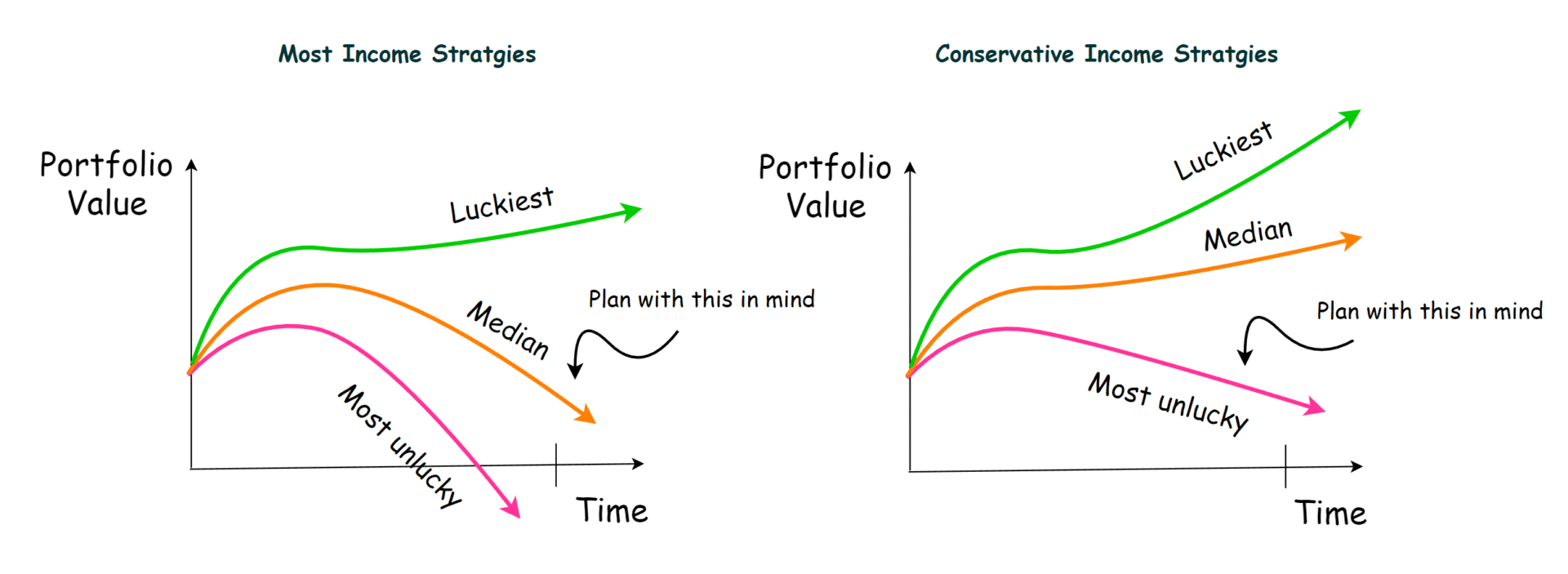

You can invest in equities, fixed income, a whole lot of different things but I want everyone to visualize your income plan in these two diagrams.

This is because since your returns is in a range of future outcomes, and inflation is also in a range, and for some your spending is in a range, your outcome can be explain in the diagram above.

Most planners will plan with median in mind.

These uncertainties you are seeing made you wonder if you are going to be the one that is more unlucky (low returns, or persistently high inflation).

And you are worried because if your plan or how you view things gets closer to the most unlucky, you end up running out of money.

The more conservative income strategy is the one to the right. You try your best to figure out the range of potential outcomes and craft a plan that when you are very unlucky, you will likely have the income you need.

Conservative plans usually end up with more capital (read money) needs.

The challenge is not everyone of us have that earnings or investment potential to accumulate so much and you would have to break your income needs into chunks and perhaps only be that conservative with the income needs that you truly want to be conservative about.

There is also a challenge about figuring out what is the range of returns and inflation. I think people beat on the safe withdrawal rate enough but it is one of the few strategies where the range of returns and inflation is tested over long time frames, but also different market returns. Not many strategies can do that.

But it is not always difficult:

- Have you look through the range of the dividend distribution over the life of STI ETF?

- What about the S&P 500?

- 99.co has the range of rental income your condo earns for the past 10 years. Have you taken a look?

So there are ways to but the question sometimes is: Can it be worse than this?

For some like the US, we have the volatility of equities and fixed income going back to the 1871. You can say that is too long ago, but what if your plan works even in those periods that doesn’t really apply? What does that say about your plan.

I think this might raise questions whether your single company can continue to distribute the income you need.

Which brings us to the last point.

3. Think About What You Don’t Want to Happen to Your Income Plan

Charlie Munger says always Invert.

And many were too focus on figuring out how to get safe returns that they failed to consider this.

The uncertainties were always there but you can’t say Donald Trump made the situation more uncertain:

- Returns aside from the US to many look more uncertain.

- We went through a pandemic five years ago where the last one was nearly a century ago.

- After a period of low inflation, we experience a period of persistently high inflation.

I think you can try to focus also on the question: If I want to pass down this income portfolio, what is the optimal setup?

I know there are those who wish to die with zero but the question forces you to consider what is needed in a longer time frame.

And in a longer time frame, returns are uncertain, inflation is uncertain, how the country move is uncertain.

If so, what is the optimal setup?

For sure it is less about the returns.

It is more about:

- Reducing the dependence on concentrated sources of returns.

- Reducing the risks of returns from single currency sources.

- Considering the potential negative sequence risk that arises from high inflation even if it is unlikely now.

- Reducing single region risks.

- Where your investments resides in.

- Liquidity

- Single star fund manager risk.

- Single income wealth manager risks.

If you want an income strategy that considers these, then you will realize the investments that gives you the highest returns might not cut it alone.

Conclusion

I nearly forgot to add one last point to the last tip:

Can this income strategy survive without you so that your beneficiaries can enjoy them?

A person with investment lens would often be in too tactical deep and never consider whether their plan can survive without them being tactical in their investments.

Is your plan foolproof even without you being tactical?

While the world looks more uncertain to some, there are those who understands their plan is built to withstand uncertainties.

And they would be wondering whether there are new uncertainties that they have not considered in their plan. Even the owner who depend on a sole Singapore condo for income may wonder if Singapore will emerge from this unchanged for the next 30 years.

That sounds like a scary risk to take on (see my Tip 3) from my point of view.

If you feel there are things that have not consider that well, hope these tips may be helpful. If you have further questions, do leave them in the comments.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

matter")